GCA FORUMS and subforums were founded with one concept in mind: To serve consumers, entrepreneurs, homebuyers, home sellers, real estate investors, and the general public. When people buy or sell a certain house, they move and, therefore, have to start life in that new place. All the partnerships that they have developed with local vendors and merchants will cease to exist ………. Read More

-

All Discussions

-

This news clip needs to be fact checked. Electric Vehicles let’s out radiation from its batteries. You will get cancer of the buttocks, testicular cancer and genital cancer from the car batteries. The batteries 🔋 of EV weighs around 10,000 pounds

-

Headline News: Wednesday, June 18, 2025

Heavy fighting flared again over Tehran today as Israel went all-out, sending warplanes to smash more than forty suspected nuclear and weapons sites. The latest barrage touched everything from centrifuge workshops to storage bunkers that engineers are thought to use night and day.

Iran Firing Back After Getting Bombed

Iran fired back with a mixed fleet of missiles and bomb-dropped drones that crossed the Persian Gulf. So far, hospital reports in Israel list zero injuries; Iranian state media have not mentioned civilian losses either.

In Jerusalem, Prime Minister Benjamin Netanyahu declared the strikes dealt a huge blow to Tehran’s atomic timetable, while in Tehran, Ayatollah Ali Khamenei warned that what he called U.S. puppets would pay dearly for a new setback.

President Trump Takes Action

Across the Atlantic, President Trump convened top advisors in the Situation Room and told reporters he might intervene or not.

Tension pushes crude prices to five-month highs, and brokers say the ripples are already shaking Wall Street. Casualty totals stand at 224 dead in Iran and 23 in the Israeli ranks, numbers that lawyers in both capitals worry will climb.

Shooting in Minnesota

Minnesota police finally cornered Vance Boelter after a sleepless 43-hour dragnet. The 57-year-old suspect is now charged with killing two state lawmakers and their spouses on June 12. His borrowed badge fooled no one once detectives discovered a stash of semiautomatics and a chilling hit list of 45 elected officials tucked under a seat.

Nation’s at Alarm Over Police Impersonators

The chilling haul has sent shock waves through Capitol halls and renewed alarms about copycat impersonators in a country frayed by partisan fury.

Los Angeles Riots

Roughly 2,000 miles southwest, Los Angeles street corners are still choked with protesters angry over ICE raids and what critics call Trumpism by decree. Rioting erupted on June 10 as part of a loose coalition labeled the No Kings movement. National Guardsmen have fanned out downtown, curfews snapped on and off like traffic signals, though most demonstrators insist they want nothing more than to march and chant. Talks between local brass and Washington law enforcement officers once stalled for days, leaving residents caught in a summer squeeze of looting, sirens, and uneasy quiet that never feels loud enough.

Trump versus Musk

President Trump and Elon Musk still get on each other’s nerves, but lately, they’ve called a truce nobody quite trusts. The real fireworks came on June 7, when Trump blasted out that their bond was over and warned Musk would pay a price if he funneled money to the Democrats. Musk shot back by labeling one of Trump’s big domestic policy bills a disgusting abomination. That jab shook the White House enough for its staff to reach out and try patching things up. Both men swallow their pride because bigger worries like war and inflation won’t disappear. Still, career officials wince whenever Musk tweets since his posts can flip government operations upside down before breakfast, and he knows it.

GCA Forums News: Real Estate and Mortgage News

The U.S. housing market feels pinched, even if single-family building permits nudged up just 0.4 percent in May to 924,000 homes. The longer story concerns the numbers nobody wants to see because new permits are slipping, which usually screams future slowdown.

Mortgage Rates

Mortgage rates dipped a fraction last week, yet they still burn a hole in any borrower’s wallet, so applications fell 2.6 percent. Prices rose only 1 percent year-over-year in May, but the inventory is so skinny that actual buyers keep getting priced out.

Home Builders

Builders who once dreamed big are quietly trimming projects and slashing sticker prices, deepening the affordability mess for first-timers.

Inflation

Inflation is wobbling right around the Federal Reserve’s 2% sweet spot, yet headlines about tariffs and new global flashpoints keep knocking the economy off balance. Most analysts figure the central bank will leave interest rates where they are when officials meet on June 18 and issue the usual 2 p.m. ET statement.

Unemployment and the Economy

Unemployment peaked at 4.2% in May, masking the quiet layoffs that emptied factory floors and retail aisles. The June payroll numbers later showed a net gain of 139,000 positions, which still paints a picture of sluggish growth while climbing oil prices add a fresh headache. Stock prices eased back in money markets, but silver surprised everyone by tagging a new peak.

Sanctuary Cities and States

A fierce legal fight is brewing over so-called sanctuary jurisdictions that refuse to help the feds round up undocumented immigrants. The Justice Department is backing a lawsuit aimed squarely at California’s sanctuary statute, and DHS has already labeled nearly 400 counties as places where federal enforcement hits roadblocks. Transportation chief Sean Duffy has warned that federal grants could vanish, a threat draws sharp rebukes from mayors such as Chicago’s Brandon Johnson, who fear it could invite troops to the streets. A list of sanctuary spots that once lived on a government web page suddenly disappeared after critics howled about being singled out.

Taxes

You’ve probably heard the buzz about red states slugging taxpayers with new levies. The funny thing is that places like Texas put $51 billion toward slashing property bills, while Florida has just wiped the sales tax off commercial leases. Governments there say the dollars are in hand, so no sweeping hikes have shown up in the books.

Trump Income Tax Overhaul

Donald Trump is still discussing extending the 2017 tax overhaul, which could sink $4.5 trillion in federal cash by 2034. He also wants to scrap the payroll bite on tips and overtime between 2025 and 2028. In January, a bill called the Fair Tax Act popped up, promising to ditch income levies, shutter the IRS, and tag a national sales tax on every purchase; so far, Congress has let it cool on the shelf. Trump rips Jerome Powell for high interest rates, yet no hard roadmap for ousting the Federal Reserve itself has ever landed on paper.

George Clooney

George Clooney recently told reporters that President Biden should step aside in the 2024 race, and of course, the cameras went wild. The out-of-the-blue remark grabbed headlines because, well, it was George Clooney. His Broadway show, a stage version of Good Night and Good Luck, keeps popping up in the write-ups, and the same is true for the story about Biden allegedly not knowing who he was when they bumped into one another. Most folks seem to shrug, saying the actor’s television whirl has nothing to do with the economy, but the star’s long-time ties to the Democratic Party still light up the news wires. Nothing else concrete from him showed up on June 18.

Gavin Newsom’s White House Bid

Out West, California Governor Gavin Newsom is eyeing a White House bid in twenty-eight. He recently slammed Donald Trump’s plan to federalize the California National Guard and blasted the former president’s immigration moves. Newsom even aired a primetime speech that reached about forty million people, trying to style himself as the face of the opposition. Oddly, he skipped the state party’s big convention that weekend, and some delegates were unhappy. His playbook sticks to bold climate rules and single-payer healthcare, yet critics keep pointing out the worsening homelessness and sky-high rent bills all across the Golden State.

What is the Latest on Kamala Harris

Kamala Harris is already sketching her next chapter now that her Secret Service detail is set to wrap up on July 21. Rumors roll between a 2028 White House bid and a 2026 return to the California governor’s mansion. In the meantime, the Vice President trades jabs with Donald Trump’s Project 2025 blueprint, warning that its proposals would put the reproductive rights of plenty of others at serious risk, and she is quietly scrubbing some of the rough edges from her public image after four challenging years in the second-highest office.

Update on Bob Menendez

Elsewhere, the news wheel keeps turning: Bob Menendez starts an eleven-year prison stretch for bribery, Lebanese pop star Elissa claims victory in a music rights lawsuit, Dodgers rookie Roki Sasaki hits pause on his throwing program because of shoulder pain, and the show Leap Day recorded another episode that has fans buzzing on social media. The scene out there feels tight, with global wars, shaky markets, and homegrown protests stacking up like storm clouds on the horizon.

-

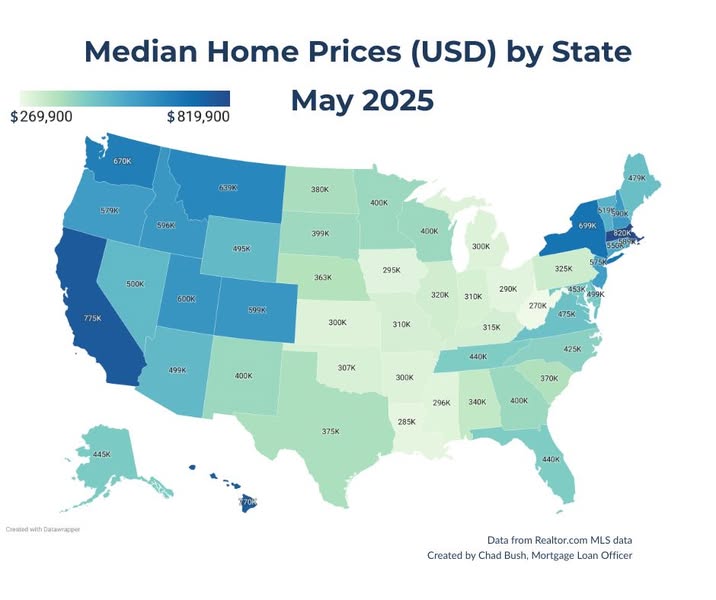

Check out this map I made showing median home prices by state for May 2025.

Is your state higher or lower than you expected?

facebook.com

Chad Bush, Mortgage Loan Officer

The Average Home Price in Your State Might Surprise You 📍 Thinking about buying a home? Here’s a quick snapshot of median home prices across the U.S. as of May 2025. You might notice some states...

-

GCA Forums News: National Roundup for June 16, 2025

Welcome back to GCA Forums News. On this Monday, June 16, we sift through police sirens blaring in Los Angeles, the latest on rent prices, a Federal Reserve meeting, faded growth predictions, and a slug of headline news that keeps rolling in.

Housing and Mortgage Market: A Stagnant Landscape

The American housing scene still feels frozen in 2025. Sky-high mortgage rates and stubborn cost-of-living bites leave most buyers and sellers staring at each other across the dinner table, unsure who should move first. Freddie Mac clocked the average 30-year-fixed mortgage at 6.84% in the week ending June 12, just a hair below last week and still hugging that 7% line we first spotted in 2022. Analysts whisper that we will drift around 6.8% for the rest of the year, with anything that looks like real relief probably sleeping until after summer.

Inventory vs. Demand

Housing listings recently hit the highest level since early 2020, yet markets feel surprisingly cool. Why? Federal Reserve of St. Louis data point to stubbornly high interest rates and an economy that still feels shaky. Many homeowners locked in mortgage rates under 5 percent refuse to move, so extra homes tend to disappear as quickly as they appear. Prices tell their own story; the Q1 2025 median home now sits at $416,900, nearly double the $208,400 recorded in Q1 2009. Real estate agents describe a frosty atmosphere; properties linger for months even in once-red-hot cities like Austin, Texas.

Renting vs. Buying

In this pricey climate, leasing looks smarter for many people. A 7 percent mortgage adds extra cost to steep prices, and monthly rent offers more wiggle room if a layoff strikes. Redfin chief economist Daryl Fairweather sums it up: Putting a down payment down feels like a gamble when paychecks could vanish in six months. On the flip side, shelter inflation of about 4 percent annually keeps pushing rents upward, pinching budgets that already squeak.

Fed Chair Powell in the Hot Seat

Jerome Powell and his team at the Federal Reserve are feeling the heat these days. When the committee met in May 2025, they chose to keep the funds rate between 4.25% and 4.5%, a choice they tucked under mixed signals and a White House still sorting out its next moves. Powell says he wants more proof and more numbers trimming those rates.

Meanwhile, President Trump isn’t hiding his frustration. The ex-president and TV real estate star Grant Cardone both blame the same high rates for dragging the housing market into the dirt. Cardone went so far as to say Powell’s course has hurt the middle class more than any previous Fed chair ever did, a claim he was glad to repeat on cable news. Trump, louder still, has demanded a one-percentage-point slash, arguing that such a cut would set off the economic fireworks voters expect. Powell, however, keeps waving the red flag about what that might do to inflation.

Interest Rate and Mortgage Rate Forecast

Because inflation increased to 2.4% in May and job growth stayed steady, most market watchers think the Federal Reserve will leave rates alone this summer. The central bank has quietly signaled that an indecisive pause beats a rushed cut when the unemployment rate sits at 4.2% and another 139,000 jobs appear on payrolls. Mortgage costs still dance to the beat of the 10-year Treasury yield, which is just over 4.4%, so homeowners should expect 30-year fixed quotes in the mid-to-upper-6 % territory until at least 2025; a broader drop to 5.5% in 2026 is only likely if inflation proves it can cool for real.

Economic Outlook: Inflation, Unemployment, and Cost of Living

The U.S. economy feels tugged in opposite directions: the jobless rate sticks at 4.2% while consumer spending slows and quarter-one growth drifts toward zero, sparking chatter about stagflation. May’s Consumer Price Index came in with a 2.4% year-over-year, slightly softer than many had braced for, but that single number still stops the Federal Reserve from crossing the threshold to cut costs. Families pay close attention to groceries, rent, and gas, and those everyday prices continue to pinch budgets even as the headline rate eases, so relief looks more like a promise than a paycheck.

Household finances still ache because rent is pricy, home loans cost a lot, and Trump-era tariffs linger. Buying a new car, snatching up a pair of jeans, or stocking the pantry has gotten trickier since 25 percent is still tacked on imports from Canada and Mexico, 55 percent from China, plus that 10 percent blanket levy across the board.

Consumer prices could nudge higher again if supplies stay squeezed and manufacturers pass on those extra charges. Economists are watching inflation numbers as baseball fans track the score in extra innings.

Wall Street and the bond pit have felt jumpy every Tuesday, Wednesday, and Thursday lately. Bad data can whiplash stocks, while good news hardly budges the 10-year Treasury yield, which refuses to settle either up or down. Money that usually pours into government notes for safety has hesitated because investors remain spooked by one injury: high inflation, high debt, and shaky jobs.

Even mortgage rates are on pause, like someone biting their tongue before making a tough call. That uncertainty keeps bond traders at arm’s length, muting buyers’ excitement.

Since swearing in again on January 20, 2025, Trump has kept his word, waving his “Big Beautiful Bill” every chance he gets. The plan could blow the federal deficit sky-high, and bond markets fear the hangover will show up in sharper yields and pricier home loans.

Critics say the tariffs pinch families hard, but supporters streak red, white, and blue, claiming the levies guard American jobs. Either way, price tags keep increasing, and the debate may outlast the sticks placed on every cargo ship at the Long Beach dock.

Trump and Musk: A Rocky Relationship

Donald Trump and Elon Musk used to trade compliments on Twitter, but the mood turned sour. On June 5, 2025, Trump blasted Musk in front of a rally crowd and called his latest project a publicity stunt nobody asked for.

Musk landed a big seat as chief of the new Department of Government Efficiency-DOGE, as the tabloids nicknamed it. Inside the tiny office, a squad of forensic auditors is combing through federal books and scanning for obvious fraud.

Curious supporters ask the same question at town halls: Where are the indictments? So far, high-profile names, such as POTUS Biden, Homeland Security head Alejandro Mayorkas, and a few others, have avoided handcuffs, and the silence is eating away at the base.

Bondi, Patel, Bongino: The Controversial Picks

Former Florida Attorney General Pam Bondi, now eyeing the A.G. seat, has defenders who love her grit but worry she can untangle the web of federal probes. Kash Patel, the short-tenured FBI chief, and Dan Bongino, a podcaster with a badge-and-briefcase past, both draw heat for resumé gaps that leap off the page. Bondi loyalists cheer her sparks on TV but admit her white-collar courtroom chops aren’t proven at the scale. Legal pros point out Patel’s days as a public defender aren’t exactly the FBI playbook, and Bongino’s decade talking into Mike’s isn’t the same as running field agents. Even tech-savvy cops note that the bureau’s toolkit has outdated the Secret Service rotation Bongino logged ten years back.

A Nation Divided

Public sentiment on Trump sits at opposite ends and shows no sign of middle ground. Fans of the president pile praise for inflation drifting to 2.3% in April, a drop many think proves his course is at least heading in the right direction. Detractors flip the script, reminding anyone who listens that promised nationwide prosecutions never arrived, and the red ink from tariffs and growing deficits still stares us in the face.

New York Attorney General Letitia James: Mortgage Fraud Allegations

Attorney General Letitia James has her eyes on mortgage fraud, hunting down lenders who may be squeezing borrowers. As of June 16, 2025, there is still radio silence on whether a federal grand jury will hand down any indictments. No headlines from the CFPB, the FBI, or the office of the U.S. Attorney General suggest the probes have moved beyond the fact-gathering stage. The public is mostly in the dark without fresh court filings or trial dates.

Los Angeles Riots: Major Headline News

LA suddenly flipped upside down on June 16, 2025, as street protests turned into full-blown riots. Early reports say sour feelings over high rents and shaky job security fuel the unrest. However, the exact spark is still unclear. Police and city officials are racing to regain control, but the scene looks slightly different every hour. Wall-to-wall cameras capture the chaos, so expect these images to dominate cable news for days.

Other Major Headlines

In a bright sports moment, the Braves piled up 19 strikeouts in a single game against the Rockies, setting a new franchise high. Spencer Strider led that charge with 13 Ks, reminding everyone why he’s the ace. Meanwhile, fans of the Immaculate Grid trivia game were chewing through puzzle 806, and several players claimed a perfect score with Wade Davis.

Messy Debate

Fans have been arguing about Lionel Messi’s appearance since joining Inter Miami. Some are gushing over his dribbles and dead-ball magic, while others blame the supporting cast for the times he looks stranded on the pitch.

Jump to June 2025:

The U.S. economy feels like a traffic jam. Housing prices barely budge while inflation keeps popping up like a stubborn weed. Washington is noisy, too; the Fed is tiptoeing, Trump is waving big tariff ideas, and TV pundits never tire of grading new cabinet picks.

Los Angeles still smolders after that brutal round of street protests, a painful reminder that unrest can break out overnight.

If you want more news, you can visit GCA Forums and refresh that tab a few times. We keep the updates rolling.

-

GCA Forums News: Housing & Mortgage Market Update – June 17, 2025

Jerome Powell and the crew at the Federal Reserve decided on June 14 to keep the overnight benchmark rate parked at 4.50 percent. Lawmakers in Washington still bicker about everything from wages to trade, and that fog makes central bankers jumpy.

Federal Reserve Holds Steady Amid Economic Uncertainty

- Just a few days earlier, President Trump blasted Powell as a numbskull from his campaign stage and demanded a 200-basis-point rate cut to save taxpayers close to $600 billion a year.

- When the economy zoomed past 5 percent growth, administration supporters looked ready to party.

- Now, they even whisper about too many thermostats affecting prices.

- Tariffs on Chinese steel and aluminum hang over the market.

- Fed researchers warn that a cheap money spree could blow the inflation balloon back in our faces.

- Most Wall Street pros now say it will take a real economic sledgehammer, a growth crash, before rates budge in either direction.

Mortgage Rate Forecast: Stability with Slight Fluctuations

Mortgage pricing barely dented this week, drifting down and then sideways as would-be buyers shuffled their feet. Freddie Mac pegs the average 30-year-fixed at 6.94 percent, while Zillow traces the rate back to June 12 and calls it roughly the same.

Market chatter says loans could bounce in a narrow band—between 6.8 percent and 7.1 percent—through the summer, with the larger economy steering most of the motion. If that forecast holds up, serious house hunters may want to lock sooner rather than later, just in case the next headline shakes things loose.

Mortgage rates are still drifting in a fog of policy talk, yet most experts think the 30-year fixed rate will hang between 6.5% and 7%. Fannie Mae has jolted its outlook upward, saying we could hit 7% by late 2025. Strangely enough, they believe those same rates might dip to around 6.3% before the last weeks of this year.

Housing Inventory Dynamics

More homes are hitting the market, shifting the power away from sellers and hinting at a summer pace that won’t feel so frantic. With rates parked at the high end, watchers guess the average mortgage will settle at roughly 6.7% come December. Policy twists from Trump and others could tangle with affordability in both predictable and wobbly ways.

Even now, the numbers look high compared to what we once thought normal. Freddie Mac’s records show the 30-year fixed rate has cruised at about 7.8% since April 1971. In that light, today’s levels still feel cheap, even if your monthly payment says otherwise.

Economic Indicators and Market Outlook

People still want houses, but there aren’t enough for sale, and mortgage payments feel heavy. The market could bounce back in 2024 even if borrowing costs stay high. The surprise run-in inflation surprised everyone in 2023, and even crazier stock swings kept buyers on the fence.

CME Group numbers show that traders now see only a one-in-five shot that the Federal Reserve slices interest rates more than twice before 2026, so don’t expect a quick policy change.

Market Implications for Mortgage Professionals

Mortgage pros feel the squeeze whenever rates jump, yet the wide-ranging market swings can hand out rare chances, too.

Key Considerations:

- Thirty-year fixed rates hover in the sturdy high-6% to low-7% band.

- Fresh inventory now fills the shelves, giving buyers genuine choice.

- Agents still need to remind shoppers that today’s numbers, rough as they seem, look mild next to the peaks of the early 1980s.

- Voices in the bond market whisper about a possible, if small, rate dip come Q4 2025.

Strategic Focus Areas:

- First-timer classes and lunchtime seminars keep younger borrowers from second-guessing themselves.

- Lofty monthly bills suddenly feel lighter if homeowners refinance once rates settle or nudge downward.

Curved-ball loan products such as 2-1 buydowns can ease the sting for clients who rely on their calculators.

- Every zip code behaves differently.

- What looks like a seller’s paradise a few miles away might feel sluggish next door.

Looking Ahead

Housing demand still flirts with bumps whenever the Fed pulls one of its mysterious levers. Brokering success means steering folks toward the long-game payoff, not the next-rate crisis tantrum.

Eyes on the calendar matter. Watch Federal Reserve meet-ups and key economic print-outs- both hold the power to twist short-term costs and, eventually, the market map itself.

The numbers in this post come straight from up-to-the-minute market feeds and a handful of analysts I trust. Mortgage pros can never rest. They must check the rates daily and peek at three or four sites before quoting a borrower.

https://www.youtube.com/watch?v=Iu_5qFoEFnY&list=RDNSSgfHDJpEgM8&index=3

-

Hi Everyone.

What are the options when a borrower has no recent rental history? For example, let’s say someone has been living in hotels for the past year, or maybe they were staying with family or friends and didn’t have rent in their name.

If the borrower has decent income, good DTI, and a low credit score around 590, how do you approach this for VA or FHA loans? Especially in cases where manual underwriting might be needed.

Can hotel stays be documented as housing history? And if they were staying with a relative, is a letter from the homeowner or utility bills in the homeowner’s name usually accepted?

Just looking to hear how others are handling these situations. Appreciate any input.

-

This discussion was modified 9 months ago by

Chad Bush.

Chad Bush.

-

This discussion was modified 9 months ago by

-

Joe Rogan—comedian, UFC commentator, and podcasting giant—continues to dominate in 2025! In this video, we take an inside look at his incredible lifestyle, from his multi-million-dollar properties to his luxurious car collection. Discover details about his wife, Jessica Ditzel, their three children, and how Rogan maintains his empire. With an ever-growing net worth, Rogan enjoys the finest things in life while staying dedicated to his passions—comedy, fitness, and thought-provoking conversations on The Joe Rogan Experience.

Stay tuned as we explore his lavish homes, top-tier vehicles, and the secrets behind his success!

-

GCA Forums News: Weekend Roundup-March 2024

Welcome to the GCA Forums Weekend Roundup for June 9-15, 2025. We put together this dispatch for home buyers, investors, loan officers, and anyone who likes to keep real estate front of mind. The stories you see below come straight from the issues our members voted on last week, so you’re reading what people want to know now. Expect solid numbers, plain talk, and no filler. In a hurry? The skimmable headlines make the whole thing move quickly, even on a busy Saturday morning.

First Stop: Mortgages

Lenders say that rates hang close to the threes, though a few early birds are already whispering about the fours. Pulling the trigger today still costs less than most wallets imagine.

Next Up is The Broader Housing Picture

According to the latest MLS snapshots, new listings are trickling out slowly, while pending sales are up almost ten points compared to last year.

Then There’s Inflation

Month-on-month price growth cooled, yet the Fed keeps flagging wage pressure as a reason to err on caution. Chair Powell told reporters that keeping the brakes on too long is a risk, but so is cutting loose before the job market settles.

Finally, the week wasn’t just numbers and forecasts. Over the weekend, an Israeli strike hit targets in Iran, a deadly shooting shook a Minnesota mall, and Senators Watz, Pritzker, and Hochul delivered fiery testimony on Capitol Hill. News cameras won’t soon forget those moments.

Mortgage Rates Nudged Up & Down

During the week of June 9-15, 2025, mortgage rates wobbled a bit as new inflation numbers and global headlines rolled in. By June 12, Freddie Mac had put the 30-year fixed rate at 6.84%, just one basis point lower than the week before, while the 15-year rate slipped to 5.97%. Around the same time, Zillow showed the longer loan stayed at 6.72% and the shorter at 5.96%, mostly reacting to news of Israeli airstrikes on Iran. Bankrate noted the 5/1 adjustable-rate mortgage hovered at 6.16%, so borrowers betting on lower rates still had some wiggle room.

What’s Coming from the Fed

Central bankers meet June 17-18, and most Wall Street watchers think they will sit tight on short-term rates. May inflation hit 2.4%, still above the 2% target, and folks aren’t seeing quick cuts thanks to stubborn price pressures and fresh talk about trade tariffs.

Lender Requirements

Fannie Mae and Freddie Mac just tightened their lending rules. Most conventional loans demand a debt-to-income (DTI) ratio below 45 percent. FHA and VA products are still kinder. They’ll back borrowers whose DTI climbs to 57 percent if strong compensating factors exist. Meanwhile, investors are discovering Non-QM and DSCR loans again. Many lenders are letting landlords skip some of the usual cash-flow paperwork.

Credit Scoring Trends

Conventional mortgages still reward anyone with a credit score above 700 with the best rates. FHA programs keep the door open at 580, which is good news for many first-time buyers. That gap between 580 and 700 lets many people cross the finish line.

Rate Forecasts

For most of 2025, the 30-year fixed rate is expected to land between 6.5 percent and 7 percent. Fannie Mae believes we might dip to 6.1 percent by New Year’s Eve if inflation cools as hoped. On the other hand, if geopolitical headaches in the Middle East send Treasury yields shooting up, those rosy predictions could head south fast.

Why It Matters

Daily rate updates are a must-read for brokers, home shoppers, and landlords alike. Investors pencil out new numbers the minute the market shifts. Refinance hunters track every tick, hoping to squeeze out extra savings. Keeping an eye on these figures gives GCA Forum members a real edge when the ground keeps moving.

Market Indicators and Housing News

As of June 2025, the U.S. housing scene has a bit of spring, even if prices still pinch first-time buyers. The Fannie Mae Home Purchase Sentiment Index hit its highest point for the year in May, hinting that folks feel a little less nervous about their finances, yet the mortgage rate hangover is far from over.

Key TrendsAffordability Challenges

The typical starter home now lists $416,900, 2.7 percent higher than a year back, so young buyers are still doing the math twice. Urban stock is tight, and although FHA and VA loans cushion some of that blow, high interest keeps the monthly number uncomfortably tall.

Housing Inventory

Suburban and rural listings crept up last month, but cities like New York and San Francisco remained painfully sparse, keeping bidding wars alive. Landlords are smiling, too. Thanks to chunky rental yields that tempt cautious investors, multi-family units are flying off the shelves.

Home Price Indices

The National Association of Realtors says pricing is steady overall, with Austin and Phoenix shining brightest for sellers in the report. Buyers hunting for bargains still find some wiggle room in places like San Francisco and Seattle, where values have begun to drift downward.

Rental Market Insights

In the rental realm, demand for multi-family buildings shot up in fast-growing Southeast metros, and that momentum shows no signs of fading. DSCR loans are helping these deals pencil out; by zeroing in on property cash flow instead of borrower income, lenders keep capital flowing to investors who want a piece of that action.

Why It Matters

Homebuyers want to know if buying now or waiting six months is smart. Sellers ask the same question in reverse. Investors keep scanning regional numbers to spot the next neighborhood on the rise.

GCA Forums zeroes in on that kind of digging. The sharp data points and plain-language breakdowns keep everyone, from mom-and-pop buyers to hedge-fund pros, clicking and talking.

Inflation and Federal Reserve Reports

The grocery store and gas pump numbers still rattle the mortgage desk. The May 2025 Consumer Price Index popped to a 2.4 percent annual pace, nudging up from 2.3 and stepping over the Fed’s clean 2 percent line.

The Personal Consumption Expenditure index, which the central bank studies the most, tells a similar story: prices are staying put longer than the officials hoped.

Federal Reserve Outlook

The Federal Open Market Committee, or FOMC, is widely seen holding its key rate in place when it gathers June 17-18. That cautious call lets the board dodge an immediate leap while it counts the economic bumps.

Some analysts blame the Trump-era tariffs and renewed Middle East flare-ups for keeping costs high.

Looking further out, the Fed is caught between rising prices on one side and climbing joblessness on the other.

Goldman Sachs now puts the odds of stagflation-consumers pulling back, growth slowing at about 45 percent, a figure rattling jittery bond traders.

Impact on Mortgages

When inflation heats up, Treasury yields usually follow, and they jumped above 1.5% after the Israeli attacks on Iran. That bump shoved mortgage rates higher almost overnight. Analysts still think a serious recession could drag those rates down again, though nothing recent points to anything below 5.5% without the economy wobbling.

Why It Matters

Home loans shape what a borrower can afford each month, and that math ripples through buying power and investment plans. Viewers of GCA Forums appreciate that when the Fed moves, their next mortgage refinance could feel it first.

Global and Domestic Events

On June 13, 2025, Israeli warplanes struck Iranian targets in a mission that rattled Wall Street. WTI crude spiked past $73.10 a barrel within hours while the benchmark 10-year Treasury yield hit 4.35%. Mortgage bonds stayed flat, but the mood on Main Street grew jittery, and further inflation could push home loan rates even higher.

Shooting in Minnesota

Information on the June shooting in Minnesota is still sketchy, with no detailed police briefings showing up in the latest files. Still, GCA Forums plans to fill that gap because neighborhood safety almost always shapes where buyers settle. Rising crime usually makes houses harder to sell, and mortgage underwriters notice long before local headlines fade.

Congressional Testimony by Senators Watz, J.B. Pritzker, and Hochul

No records show whether Senators Watz, J.B. Pritzker, and Governor Kathy Hochul spoke in front of Congress between June 9 and June 15, 2025. Still, people following housing news guessed topics like affordable rent, stimulus money, or new roads were on the table. Pritzker and Hochul often pushed bills that fit those headlines so their appearance would have caught the cameras. Anyone logging into GCA Forums the morning after would likely find clips shaking up the real-estate feed.

The Headline News Weekend Edition from GCA Forums packs everything home shoppers and lenders crave by mid-June: the latest mortgage rate dip, inflation whispers, Fed signals, plus a haunting note on the Israeli bombing of Iran. Fannie Mae updates and National Association of Realtors numbers sit alongside August polls from Pew. For investors trying to stay ahead, these five minutes are more useful than a stack of quarterly reports. Could you check the site tomorrow? The market moves while most phones are asleep.

-

GCA Forums News: National Update for Friday, June 13, 2025

Welcome to GCA Forums News. We look across the country in June, from the troubled housing market to the breaking Los Angeles riots. If you need the headlines fast, you are in the right place.

Housing and Mortgage News

- High mortgage rates, stubbornly set near 6.89 percent, keep many buyers on the sidelines.

- Freddie Mac numbers from June 12 show a tiny dip from 6.97, yet the relief feels thin.

- Redfin reports about half a million more buyers than homes for sale.

- Weighted by that gap, the median house price of $416,900 in the first quarter is still out of reach for nurses, teachers, and recent grads.

- Fannie Mae expects a full-year slide toward 6.1 percent and 5.8 percent heading into 2026.

- Redfin hedges lower, and the rest of 2025 will be around 6.8.

- Most economists, however, warn borrowers hoping for a dip below 5.5 are waiting on a recession that no one truly wants.

Renting vs. Buying

- People eyeing a new place are staring at sky-high mortgage rates, so renting starts to look like the smarter move.

- Bright MLS says prices are still increasing, but not fast enough for buyers to call the shots.

- In the priciest cities, the monthly rent often beats the math on a 30-year loan.

Feds Watchlist

- Jerome Powell and his crew at the Federal Reserve feel the heat from every corner.

- The May 2025 policy meeting ended with the funds rate at 4.25 to 4.50 percent because the inflation and job numbers won’t sit.

Future Rate Moves

- Most Wall Street pros, including the folks at Citibank, don’t see any cuts before the September calendar rolls around.

- Powell keeps saying the decision depends on the next batch of data, no matter what politicians shout out.

- President Trump and FHFA head William Pulte are still waving the cut-them-now banner, yet the Chair stays cool.

Tariff Clouds

- Powell keeps the tariff talk in his back pocket, admitting that Washington duty games could pinch growth while pushing prices higher.

- The clock is ticking on the rumored 90-day reset, and every tick adds noise to bond yields.

Critics Circle

- Real-estate magnate Grant Cardone is never shy; he calls the rate freeze a flat-out housing disaster.

- Pulte jumps in, echoing that the high Fed line is icing the market for most home shoppers.

Economic Snapshot

- The latest scoreboards are mixed.

- May CPI showed prices creeping up again.

- The Kansas City branch predicts 3.2 percent for the year, well over that 2 percent comfort mark the Fed brags about at the meeting.

Unemployment and Job Growth

- April 2025 welcomed 177,000 new non-farm payrolls, a pleasant surprise that beat most forecasts.

- The unemployment rate held steady at 4.2%, though a lean 37,000 added to private payrolls planted a few seeds of worry.

Cost of Living

- Recent tariffs on imported goods have some experts warning that prices of electric bills could jump again.

- Consumer spending looked tired in the first quarter, and early estimates show GDP growth slowed from the previous pace.

Stock and Bond Markets

- The yield on the 10-year Treasury slipped to 0.62%, easing the anxiety of anxious home shoppers by lowering mortgage rates a notch.

- Even so, trading floors feel jumpy because nobody can predict tomorrow’s tariff announcement.

Letitia James Mortgage Fraud Allegations

- New York Attorney General Letitia James is now at the center of a federal mortgage fraud inquiry.

- FBI agents working under Director Kash Patel and his deputy, Dan Bongino, are conducting the probe.

Investigation Progress

- A grand jury in Virginia’s Eastern District has already sent out subpoenas.

- James insists the scrutiny is payback for her $455 million win over Trump.

- As of June 13, 2025, he faces no charges, indictments, or set trial dates.

CFPB and DOJ Involvement

- The Consumer Financial Protection Bureau, now under the supervision of Justice Department Inspector General Michael Horowitz, investigates potential consumer harm.

- Attorney General Pam Bondi has made the case a top DOJ priority.

Public Sentiment

- James plans to fund her legal defense with private and state money, a decision critics say smells of political maneuvering.

- Public opinion remains split, with supporters praising her toughness and detractors shouting foul play.

Real Estate and Mortgage Industry

- Right now, the housing market feels stuck.

- Mortgage rates are high, so homeowners skip refinancing, and sales volume is flat.

- Gustan Cho Associates, famous for its hands-on FHA and VA underwriting, keeps hearing from borrowers with bruised credit and even folks in Chapter 7 bankruptcy.

- That steady traffic proves demand never really disappears.

- More inventory is showing up on listing sheets.

- Buyers in the market enjoy extra wiggle room, yet prices barely budge enough to jump-start movement.

- Non-QM loans are finding a niche for self-employed workers and others who don’t fit the QM narrow box.

- The catch, of course, is a heftier down payment that some families don’t have.

Trump Administration and Cabinet

- President Trump is still trying to check off big campaign promises six months in, and more than a few voters are counting.

- His tariffs may cheer factory owners, but critics want to see the indictments that keep getting hinted at.

- Trump and Elon Musk are no longer sparring on Twitter.

- They are teaming up in Washington, too.

- Musk’s new Department of Government Efficiency- DOGE, everyone is calling it, claims it has uncovered waste that would make accountants gasp.

- The centerpiece, a sprawling reform nicknamed the Big Beautiful Bill, has yet to hit a single markup.

- Staffers parade maps and flowcharts in and out of the Oval Office, but real legislative draft ink is still dry.

- Inside the Justice Department, Pam Bondi draws sharp lines.

- Her brisk pace on the James probe matches Trump’s tone, yet it raises flags about whether the law is being enforced or choreographed.

Conflict at the Top

- FBI insiders are nervous after Kash Patel and Dan Bongino slid into the director’s chairs.

- They say Patel has never tried a criminal case, and Bongino hasn’t worn a badge in years.

- Law staffers complain the pair don’t have the courtroom chops to keep the agency’s word.

Still No Handcuffs

- Campaign trail bluster promised busts for the Biden clan, Secretary Mayorkas, and Dr. Fauci, yet the grand jury’s silence is deafening.

- DOGE’s forensic teams are still sifting through paper, but show nothing the public can grab.

L.A. in Flames

- Los Angeles streets are burning as of June 13, 2025.

- Local papers hint at police shortages or a new celebrity scandal.

- Still, nobody can pin the match that lit the fuse.

- NATIONAL GAZETTE and even cable networks are strangely quiet on the flashpoints.

Odds and Ends

- Bond traders are jittery because former President Trump just tossed fresh China tariffs back onto the table.

- Powell v. Federal Board landed yesterday, and the Justices said Jay Powell can’t be fired at a whim.

- That move buys the Fed more leeway.

- Stagflation worries keep shoppers grim, and layoffs are now more headline than rumor.

Big Picture

- Housing sales are stuck in the mud, mortgage notes are back to 7 percent, and voters feel the squeeze.

- The Letitia James probe is getting louder, and critics still slam Trump for cabinet picks that look light on experience and heavy on a promise.

- GCA Forums News will ring your phone if anything moves.

Got a quick mortgage question? Gustan Cho Associates answers phones and emails quickly. Dial 800-900-8569 or email alex@gustancho.com, and someone will jump in.

- Federal Reserve chair Jerome Powell warns that inflation is hotter than a Thanksgiving turkey.

- Headlines rumble about Trump tariffs that could push lumber back into orbit.

- New York AG Letitia James is busy unraveling tales of mortgage fraud.

- When rent is due and budgets are tight, many folks weigh renting vs. buying with anxious calculators.

- An unemployment tick-up or down changes everybody’s housing plans.

- Seasoned watchers recall how the Trump administration’s policies made both waves and calm in the markets.

- Kash Patel and Dan Bongino still trade barbs on cable.

- At the same time, the Los Angeles riots linger in the memory of investors.

- Even Congress joins the chatter, throwing around phrases like the Big Beautiful Bill.

- Tech titan Elon Musk swings between backing wild ideas and cozying up to Trump.

- Between all that, mortgage rates hover, nudging the price tags on starter homes.

- Stock market volatility never sleeps, and neither do the blogs trying to explain why.

- Today’s buzzword is housing market 2025, a date that feels close yet very far.

-

Always wondered what happened to Mike Lindell. Could you please provide a comprehensive overview of what happened between Mike Lindell, the founder of MyPillow, and former President Donald Trump? During Trump’s first term in office, Lindell was known as one of his most loyal supporters. He often visited the White House and even spent money defending Trump. Their relationship seemed exceptionally close, with Lindell fully committed to supporting the President.

However, there have been many conflicting reports about Mike Lindell recently — not just small contradictions, but major shifts. For example, I heard that Lindell was recently hit with a $9 million debt bill. After promoting claims that the Democrats, Joe Biden, and Kamala Harris stole the 2020 election, Lindell’s company, MyPillow, faced widespread consumer boycotts. Additionally, Lindell has been the target of multiple lawsuits related to his election fraud claims. Notably, FedEx is suing MyPillow for breach of contract and unjust enrichment, seeking to collect nearly $9 million for unpaid shipping services.

The lawsuit details that MyPillow and its predecessor company, MP Distribution, LLC, entered a Transportation Services Agreement with FedEx in February 2021. Over the next few years, the contract was amended several times to adjust pricing and accommodate changes requested by MyPillow representatives.

With all this background in mind, could you also share a detailed biography of Mike Lindell? Please include his childhood, upbringing, education, parents and siblings, early work history, first job, and how he started his businesses. I’d also like to know how Mike Lindell became close to President Trump, what has transpired between them since, why Lindell appears to be so quiet about Trump now, why he was not involved in Trump’s most recent campaign, whether Mike Lindell is okay, and what he is currently doing.

-

This discussion was modified 10 months, 3 weeks ago by

Lilly.

Lilly.

-

This discussion was modified 10 months, 3 weeks ago by

Gustan Cho.

Gustan Cho.

-

This discussion was modified 10 months, 3 weeks ago by Gustan Cho.

-

This discussion was modified 10 months, 3 weeks ago by

-

♪♫♬ Lady Gaga – Always Remember Us This Way ♪♫♬

I do not own anything. All credits go to the right owners. No copyright intended.

Lady Gaga – Always Remember Us This Way ( Lyrics Video ) Words:

That Arizona sky burning in your eyes

You look at me and, babe, I wanna catch on fire

It’s buried in my soul like California gold

You found the light in me that I couldn’t findSo when I’m all choked up

But I can’t find the words

Every time we say goodbye

Baby, it hurts

When the sun goes down

And the band won’t play

I’ll always remember us this wayLovers in the night

Poets trying to write

We don’t know how to rhyme

But, damn, we try

But all I really know

You’re where I wanna go

The part of me that’s you will never dieSo when I’m all choked up

But I can’t find the words

Every time we say goodbye

Baby, it hurts

When the sun goes down

And the band won’t play

I’ll always remember us this wayOh, yeah

I don’t wanna be just a memory, baby, yeahWhen I’m all choked up

But I can’t find the words

Every time we say goodbye

Baby, it hurts

When the sun goes down

And the band won’t play

I’ll always remember us this way, oh, yeahWhen you look at me

And the whole world fades

I’ll always remember us this wayCopyright Disclaimer Under Section 107 of the Copyright Act 1976, allowance is made for “fair use” for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use is a use permitted by copyright statute that might otherwise be infringing. Non-profit, educational or personal use tips the balance in favor of fair use.

Thanks for Watching 🙂

https://youtu.be/5vheNbQlsyU?si=TBZk97mNpVp26Cu2 -

On today’s edition of GCA Forums News for Wednesday, June 11, 2025, we will cover the following important trending topics:

1. We will update our viewers on the latest fiasco between President Donald J. Trump and Elon Musk.

2. We will cover if the relationship between Trump and Musk will ever reconcile or if this is the END of a fast-paced new friendship and alliance. Musk keeps on saying that Trump is on Epstein’s pedophile flight log which Trump vehemently denies.

3. We will cover the Los Angeles riots and the feud between Trump, Tom Homan, and California Governor Gavin Newsom and contemplate the theory that Newsom is trying to stir up political chaos, civil war, and divisions against Trump because he has an ulterior motive to gain brownie points and get ahead in the 2028 Presidential election. Kamala Harris has not announced she will run for the office of Governor of California.

4. We will cover Trump’s Big Beautiful Bill. Fellow Republican senators seem to be more opposed. Remember that the Big Beautiful Bill barely passed the House by one vote. Now, with several Republican senators against the bill, Trump has a long, dim road ahead trying to make it into law.

5. The economy and job market are awful. Many Americans either have or are expecting to lose their jobs with no promising employment in the future. The U.S. economy is on life support, and Wall Street is in denial, where the DJIA is swinging upwards by triple digits and tanking the same. The volatility in the stock market signals that the stock and bond markets are clueless..

7. We will thoroughly examine inflation, the Federal Reserve Board’s potential cuts in interest rates and mortgage rates, housing inventory, home prices, and the overall housing and mortgage markets.

8. What is going on with sanctuary cities and sanctuary states? Illinois Governor JB Pritzker is in Washington on a conference with lawmakers concerning offering a haven to illegal migrants and discussing sanctuary cities and states, as well as the federal government cutting federal funding dollars to states that are proclaimed sanctuary cities and sanctuary states.

9. What are the updates on mayors, judges, and politicians shielding illegal migrants from Federal Immigration and Customs Enforcement agents? What is the latest on Congressman Hakim Jeffreys that he will publicly name all federal ICE agents who are rounding up illegal migrants and deporting them?

10. Is Elon Musk’s Department of Government Efficiency completely dead? Is there any way to cut billions of dollars of wasteful spending? Why are U.S. Attorney General Pam Bondi and FBI Director Kash Patel dragging their feet when filing charges on the Biden Administration’s wrongdoings? Are the pardons and commutations signed with the auto pen null and void, or will nothing happen with that, too? Senator Adam Schiff, former Congresswoman Liz Cheney, Dr. Anthony Fauci, Barack Obama, Bill Gates, Hillary and Bill Clinton, Andrew Cuomo, Hunter Biden, Joe Biden, Dominion voting machines, and hundreds if not thousands of people of power who committed crimes and crimes against humanity needs to get charged, arrested, tried, and sentenced to prison for a long time. Pam Bondi and Kash Patel are either completely incompetent, lazy, or not thinking about doing anything. Why aren’t these corrupt judges getting charged, arrested, tried, and sentenced? Why are they not being put in their places? What is the latest on New York Attorney General Letitia James and Fulton County, Georgia District Attorney Fani Willis?

We will give you a comprehensive detailed report on the topics from above and more. Stay tuned.

https://www.youtube.com/watch?v=wXMEF63N3N8&list=RDNSwXMEF63N3N8&start_radio=1

-

Hey there, and welcome to the Thursday, June 12, 2025, edition of GCA Forums News. Glad you could stop by!

Mortgage Market, Fed Moves, and Housing Buzz: June 12, 2025

June is already humming along with headlines no one wants to miss. If mortgages, the Federal Reserve, and the place we call home pop into your mind, you aren’t alone.

Federal Reserve Talk

- Jerome Powell stepped back into the spotlight yesterday and pulled no punches.

- He reminded Wall Street that the Fed watches interest rates like a hawk.

- I plan to go straight to the big point: there are no rate cuts yet.

- Surging inflation still scares them, so every hint Powell dropped landed in the cautious camp.

Mortgage Rates Update

- Mortgage lenders are jittery, and that shows up in the window.

- Today, the average 30-year fixed is around 7.25 percent, up from 7.15 percent just last week.

- Whether that trend sticks depends on how markets digest tomorrow’s employment report.

- Bad numbers could push rates even higher, while a strong jobs boost might relax lenders for a minute or two.

Housing Inventory vs. Demand

- Housing inventory flatlines at just under 1 million single-family homes, a number that has derailed first-time buyers for months.

- Demand, however, sits stubbornly high thanks to Millennials hitting their purchasing stride.

- Economists keep calling the market stale, yet bidding wars still pop up in cities like Austin and Raleigh.

- That odd mix of cold headlines and hot offers keeps everyone scratching their heads.

NY AG Letitia James and Fraud Allegations

- Eyes are glued to New York Attorney General Letitia James, who dropped mortgage fraud allegations that read like a spy novel.

- The CFPB, FBI, and U.S. Attorney General Merrick Garland are now elbow-deep in paper.

- Rumors swirl that a federal grand jury could be seated by the end of the month.

Prosecutors want air-tight files before any jury is sworn in, which slows the gossip but speeds up the paperwork.

Rent vs. Buy Dilemma

- Renters still face sky-high landlords charging 25 percent more than two years ago, while buyers grind through high rates.

- That classic rent-versus-buy debate feels less like a debate and more like a math problem few can solve.

Economy Snapshots

- Unemployment has dipped to 4.3 percent, yet plenty of gig workers say the safety net feels threadbare.

- Job growth continues, especially in the renewable sector, but wages trail inflation like a puppy on a short leash.

- The cost of living is highest in the real estate corridor from San Francisco to Boston, where even a loaf of bread can cause buyers to regret it.

- Grocers blame supply chains, and landlords blame lenders, so the blame circle spins on.

Stock and Bond Market Rollercoaster

- Bond yields jumped after Powell spoke, sending mortgage-backed securities into a tailspin.

- Stocks hesitated, then rallied, hoping any rate rise would be tiny.

- Volatility is the new black, and portfolios either love or hate it.

Tariffs and Trump

- Still, the headline magnet, Trump nudged tariffs on steel and lumber back into the conversation.

- Builders suspect the White House wants to lower prices, while manufacturers worry it’ll backfire.\

- Meanwhile, his bond with Elon Musk skips the line between cooperation on space and friction on taxes.

- Musk, ever the public thinker, hints at chat about electric truck production only when the tariff fog clears.

Big Beautiful Bill and Cabinet Crew

- The Big Beautiful Bill, another name for Trump’s latest infrastructure pitch, is poised for summer debate.

- The new Attorney General, Pam Bondi, says justice will oversee enforcement.

- Kash Patel sings the same tune in the FBI, though skeptics wonder if talk beats walk.

- Dan Bongino, the deputy director who is no stranger to media fire, insists the agency is in the weeds tracking fentanyl and Wall Street mischief, not Twitter feuds.

American Confidence

- Americans split in polls about Trump’s leadership, yet confidence numbers wobble less than you’d think.

- Group chats on cable news blur the lines between praise and panic, giving pundits plenty to shout about.

- The biggest question is whether that confidence can translate to a landscape free of real estate heartburn or mortgage surprise.

- Plenty of lawyers and law-adjacent pros are speaking up and saying Kash Patel and Dan Bongino aren’t the right fit for the top two slots at the FBI.

- They think we need someone with deeper chops before the Bureau gets a new helm.

- Patel briefly stretched as a public defender and bounced between government gigs.

- Still, most folks agree that a track record isn’t enough if you’re taking the director’s chair.

- Bongino hosts a high-energy podcast and leans hard to the right, so his name rings alarm bells for many career agents.

- He logged a few years as a beat cop in New York, then guarded Barack Obama as a Secret Service screener, yet those jobs leave a big gap when the Bureau looks for its number two.

- More than ten years have passed since the agency hit the reset button on its tech and chain of command.

- Dan Bongino, once part of that world, has tried and failed to win office in Maryland and Florida.

- Lately, he spends his days behind a YouTube mic or posting on Rumble and Facebook, and he pops up on other channels chasing the same audience.

- July 2025 is creeping up on us. Donald Trump took the White House again on November 5, 2024.

- Half a year into his second term, the promised handcuffs for what some call the Biden-domiciled swamp still dangle in mid-air.

- No blockbuster indictments, no headline-making arrests.

- People keep asking, Who exactly?

- Fair question.

- Maybe the so-called Biden Crime Family, Alejandro Mayorkas at Homeland Security, or Congressman Adam Schiff.

- Some even toss Dr. Anthony Fauci, ex-New York Governor Andrew Cuomo, and Bill Gates, whose talk of limiting population keeps sparking arguments.

- Barack Obama, Bill Clinton, and the former Secretary of State, Hillary Rodham Clinton, all share headlines more often than they probably enjoy.

- A horde of unnamed celebrities, certain disgraced members of Congress like Liz Cheney and Matt Kisinger who still rub folks the wrong way, plus everyone connected to January 6, 2001.

Elon Musk, now obsessed with cleaning D.C. messes, says his data-wrangling crew turned up fingerprints that look like fraud against taxpayers.

The L.A. riots—a flashpoint no one can forget—kept breaking on GCA Forums News the afternoon of June 12, 2025, with tapes and eyewitness posts flooding in before dinner.

https://www.youtube.com/watch?v=H7vmtBeh5AM&list=RDNSwXMEF63N3N8&index=3

-

Can you get charged for a DUI in Illinois if you are parked and are sitting in your car without the engine running?

-

Should I get section 8 or market rent tenants for my investment properties? What are the pros and cons having tenants with section 8 vouchers or market rent tenants?

-

We will discuss the Jeep Gladiator in this post. Talk about gas vs diesel, the different trim levels, and the customability potential with the Jeep Gladiator. There are so many after market accessories available on the Jeep Gladiators than any other trucks. From soft vs hard tops, painted vs black fender flares, lift kits, paint options, stock vs custom trim levels, wheels and tires, exterior and interior accessories and options, electrical and electronic equipment options, engine and power options, consumer reviews, and most importantly, comparison between the Jeep Gladiator versus other Jeep brands. We will go over the pros and cons of the countless modification options available in the marketplace. Other topics covered is the five foot bed, off road ability of the Jeep Gladiator, using the Jeep Gladiator for pleasure versus using the truck as a work truck.

We will cover the engine options available for Jeep Gladiators. The Jeep Gladiator has a unique look compared to other trucks.

I replaced my Gladiator with a Ram Rebel! : • 18 Months with the Ram…

I bought my 2021 Jeep Gladiator one year ago and it’s time for a full review. This comes from an actual owner, I have zero affiliation with Jeep. Why did I choose a Gladiator over the competition? Does it live up to the promise of combining the off-road ability of the Jeep Wrangler with the utility and towing ability of a pickup truck? THIS is an honest OWNER review of the Jeep Gladiator.

I chose the Gladiator instead of it’s competition: Toyota Tacoma, Nissan Frontier, Ford Ranger, Jeep Wrangler, Toyota 4Runner, Ford F-150, Toyota Tundra, RAM 1500, Chevy Silverado, GMC Sierra, Nissan Titan, Ford Bronco, Chevy Colorado, GMC Canyon, Honda Ridgeline.

-

I have been hearing and also know a few friends and co-workers who are Jeep lovers and swear that Jeeps are great investments, especially the older Jeeps, where you can restore and make the Jeep look like new. Many Jeeps from the 1980s, especially the Jeep Wrangler Rubicon, are great investments if you buy them at the right price and are mechanically sound and in excellent shape and have been well taken care of, preferably garaged. If any viewers and members of Great Community Authority Forums and Sub-Forums are Jeep experts and Jeep lovers, if you can guide us through the various types of Jeeps and suggest and recommend what type of Jeeps to look out for and what type of Jeeps to stay away from, it would be largely appreciated. I have five large dogs and my dogs always travel together with me when running errands and when I need to go to my office. How is the space of 4 door Jeeps? From the picture, it looks cramped and not too spacious. What Jeep would you recommend for folks with multiple large dogs.

Attached is a video clip by Dennis Collins talk about 1981 to 1986 Jeep CJ. Some of these Jeeps have appreciated crazy in value.

Welcome to Coffee Walk Ep. 147!

This week we’re talking Jeep CJ’s and how to tell the difference(s) between a Base, Renegade, Laredo and a Limited Edition Model. Let me know which Jeep is your favorite in the comments section below AND let me know if this killer CJ collection that we’ve been stacking up over at our secret warehouse is something that you guys would like for us to feature on an episode here soon… although, I think I may already know the answer to Question #2!As always… GO FAST, HAVE FUN & HAVE A GREAT WEEKEND!! and thanks for watching!

-

There are now nearly 500,000 more homes for sale than buyers actively looking. See what that can mean for you.

instagram.com

3 likes, 0 comments - chadbushrealestate on June 5, 2025: "Buyer's Market: More Sellers, More Options Nearly 500,000 More Homes for Sale Than Buyers, Here’s What It Means for You Right now, there are almost half a million more sellers … Continue reading

-

Electric Vehicles or EVs were the nation’s talk, especially among Democrats. Many states, like California, have mandated that electric vehicles be the vehicle of choice by a certain year, and consumers will no longer be allowed to drive gas-powered vehicles. However, electric vehicles have been launched and are in full production. There are a lot of kinks and things wrong with electric vehicles. Tesla’s Cyber Truck was the gem of Elon Musk and considered the pinnacle of EVs. However, the Cyber Truck costs over $100,000, and values have plummeted within months of a buyer purchasing the Cyber Truck. At first, Tesla’s Cyber Truck sold for a big premium over the MSRP. For example, some consumers purchased Tesla’s electric vehicles for almost $200,000, and in less than one year, the Tesla Cyber Truck is valued at $60,000. Many people are skittish about buying a used electric vehicle because the battery panel of the EV is the heart and brain of all electric vehicles. The battery power source alone can cost over $50,000, and the battery has been proven to it can go bad in five years. With a battery needing replacing on an electric vehicle, the vehicle is worthless. Electric vehicles were expected to be a hit and very popular, exceeding gas-powered vehicles in production. Unfortunately, many EV owners threw in the towel and took the loss of selling their electric vehicle and trading it in for a gas-powered vehicle. Shaque O’Neill purchased three Tesla Cyber Trucks less than one year ago. After Elon Musk and President Trump had a big argument, Shaque O’Neill sold all three Tesla Aluminum Cyber Trucks. Plus, the infrastructure of the EV charging systems throughout the country is in its infancy, and the country is not ready to adjust and turn in its gas-powered vehicles for electric vehicles.

-

We will cover today’s comprehensive daily news in today’s GCA Forums News for Monday, June 9, 2025. We will cover the latest update between President Trump and Elon Musk. Last week, there was a major blowout between Trump and Musk. Trump and his inner circle no longer trust Musk. Musk invested millions in Trump, but what is the real story? Did Musk have an ulterior motive? Is Tesla deteriorating? Tesla’s Cyber truck is sitting dormant and not selling. The left loved Musk but no longer after he supported Trump and the Republicans. What is going on with the latest housing and mortgage news? What is happening with the Dow Jones Industrial Average, other indices, and Tesla stock? Tesla stock lost 14% last Thursday. Musk got kicked out of the White House. What is going on with Trump’s Tariffs? What is going on with precious metals? What is the latest with inflation? Did Trump use Musk and leave him after he used Musk? What is going on with the economy? What is going on with both sides of the political spectrum? What is going on with the Department of Government Efficiency? Is this the end of Elon Musk? Did the public turn its back on Musk?

GCA Forums News: Monday, June 9, 2025

Update on Trump-Musk Romance

The relationship between President Trump and Musk has degenerated into a public feud, escalating rather rapidly last week. On Trump’s part, it started on June 5, 2025, when he threatened to cut government contracts and subsidies for Musk’s companies, including Tesla and SpaceX, which he claimed could cost billions.

Accusations by Musk

- In retaliation, Musk accused Trump of running his economy into the ground, pledging a recession in the second half of 2025 at Trump’s hands.

- He even called for bursting Trump’s impeachment balloon and idly tweeted about SpaceX’s Dragon spacecraft being decommissioned—while cautioning, later, that he’d retract.

- Elon Musk intensified his social media attacks on Trump, doubled down on his reframing, and focused even more on claiming Trump’s policies had destroyed American quality of life.

- Musk claimed he should be outraged, describing this as unprecedented.

- How in a democracy someone can be de facto ruled by a person suffering from the character divide seemed immeasurable when Musk turned against Trump for his tax and spending policies, declaring them “stuffed with disgusting pork” and demanding from his followers on X that Congress kill them.

- It would be hard to forget how, together in May and March of 2025, they attended Disneyland and sipped drinks here and there while seated on couches in Trump’s cab after participating in joint dinners where they proposed spending bills.

- Musk’s critics argued that he wanted to control policy to benefit Tesla and SpaceX, which depend on federal contracts and subsidies.

- The Washington Post estimated that Musk’s companies receive approximately $38 billion of federal spending.

- Out of that, SpaceX alone constituted $22 billion. Despite this, Musk’s vocal criticisms of Trump suggest he did not expect Trump to accommodate his influence, and his attempts at accommodating Musk may have backfired.

- No concrete evidence goes beyond the stated reason for downsizing the government, for Musk’s sudden fallout with Trump, which raises questions of strategy gone wrong.

Did Trump use Musk?

- Trump’s embrace of Musk, starting with giving him the position of leading DOGE and showcasing Tesla vehicles at the White House, was a public display of approval.

- After Musk criticized Trump, the latter distanced himself, saying he was “disappointed,” which many interpreted as suggesting that Musk’s exit from DOGE was due to his inability to handle the role.

- Some House Republicans also voiced dissatisfaction with Musk’s supposed lackluster performance in the role.

- However, it seems more likely that Trump used Musk’s influence to achieve his objectives and shut him out when they no longer aligned.

Tesla’s Performance and Cybertruck Sales

- On June 5, 2025, Tesla’s stock plummeted 14.3%, erasing its value by 150 billion dollars, marking the largest single-day drop in history.

- The decline was caused by the Musk-Trump feud, specifically Trump’s threatened removal of EV tax credits, which would have netted Tesla $1.2 billion.

- Tesla’s stock price experienced a minor recovery on June 6.

- Still, it remained down 21% in 2025 and had experienced a 33% decline since Trump’s inauguration.

Sales of Cybertrucks:

- Tesla is not doing well in Cybertruck sales, as analysts point toward Musk’s prioritization of this model over more utilitarian vehicles as a bigger drag on sales.

- Total sales of Tesla vehicles have also declined partly due to Musk’s political activism, which led to protests at Tesla plants in the US and Europe.

- In the EU, sales are down because of the political backlash, while in China, Tesla faces steep competition from domestic EV manufacturers.

- These factors, along with the anticipated withdrawal of federal aid, put Tesla in a weaker position in the market.

Perception of Government and Politics

- Musk’s shift from a revered leftist tech figure to a Trump Republican has cost him a lot of goodwill.

- According to X posts, his net favorability has shifted from +24 to -19 points, with a staggering 126-point drop among Democrats.

- The backlash against Musk has also affected Tesla, with a dip of 20 in net favorability.

- Musk has recently come under fire from the left sympathizers who used to endorse him because of his green energy innovations.

- Now, he is considered disloyal for backing Trump.

- On the other hand, some Republicans question his loyalty due to his reprimands for Trump’s policies.

Is This the End of Musk?

Despite these recent conflicts, Musk remains the world’s richest man. SpaceX and Tesla play integral roles in the United States space industry and the electric vehicle market. Due to government contracts, complete dismemberment is mostly impossible. Still, his political blunders and divided focus have hurt his public image and Tesla’s market performance. Musk’s crisis management will have to focus on stabilizing Tesla alongside maintaining government partnerships for SpaceX.

Trump’s Tariffs

- Concerns about economic fallout have surged due to Trump’s aggressive policies on tariffs.

- These include a proposed 50% tariff on certain European goods and the China trade war.

- Tariffs often trigger a recession or, at the very least, stagnate growth.

- Analysts fear that these tariffs will spur inflation and disrupt international trade, a view Musk has vocally supported.

- On June 5, a phone call between Trump and Xi brought some optimism toward progress in tariff negotiations.

- However, nothing of substance has been done. The complete economic impact of these tariffs is anticipated to become much clearer in the following months.

Recent Mortgage and Housing Updates

The first dip in mortgage rates after a month, Treasury yields led to a fall. Mortgage rates are now at 6.9%. These rates continue to dampen homebuying activity, especially during the important spring period. The housing market faces wider economic uncertainty due to tariffs, federal funding cuts, and decreased government spending.

Summary of the Dow Jones Industrial Average and Other Indices

- The Dow Jones Industrial Average, on 6/6/2025, jumped over 400 points (1.1%) to 42,319.74, closing above 42K for the first time.

- This resulted in a new high for NASDAQ for the year, sitting at around 6k.

- SP500 also rose above 6000, indicating a bullish market sentiment.

- May job figures showing surprising improvement and some signs of a truce in the ongoing feud involving Trump and Musk were the reasons for this rally.

- On the other hand, markets were dipping ahead of June 5, with Tesla’s induced slump alongside uncertainty around tariffs pushing the Dow lower by 0.25%, while SP500 and NASDAQ tracked it down with declines of 0.5% and 0.8%, respectively.

Precious metals update

Concerns regarding tariffs have incentivized investors to turn to gold, silver, and platinum, which, as of June 6, have reached multi-year highs surpassing prices observed previously. While we lack specific data points, the trend indicates a growing unease about inflation and trade tensions.

Inflation Update

- Concerns related to inflation have mounted to a good extent due to the tariffs imposed by Trump.

- Based on regional inflation rates, President Jeff Schmid of the Kansas City Federal Reserve claimed on June 5 that tariffs would reignite inflation.

- He warned that their impact could be felt within months.

- China’s producer deflation contracted at the worst rate in nearly two years in May, which shows how dire the global economy is facing.

- The Federal Reserve is still cautious about slashing rates as job data remain unchanged, and the effects of tariffs are yet to be fully captured within the numbers.

Department of Government Efficiency (DOGE)

- DOGE, or Department of Government Efficiency, was created and headed by Musk as an initiative to reduce the Federal workforce and government spending and fire several contractors.

- Musk’s abrupt exit came after he classified himself as ineffective under the Trump administration.

- With no clear successor announced yet, Trump’s remarks indicate that he no longer hopes to rely on Musk’s input amid other comments criticizing Trump’s last-minute decisions.

Economic Outlook

- Reduced federal funding, imposed tariffs, and stagnant spending will heavily strain the economy.

- By laying off nearly 100,000 employees in May, U.S. employers exacerbated job cuts for 2025 to below 700,000 while increasing their rate by 47% yearly.

- This makes for a disturbing economic cocktail, especially when combined with the projected costs of increasing inflation due to tariffs.

- This prediction contrasts with Musk’s expectation of recession-inspired growth.

Meanwhile, the XX CNN and Quartz links tell of a northern trigger that surfaced across markets and did not end well. Regardless, the Tesla market value is intricately tied to Elon as both are public figures’ faces and are somewhat expected to be hurt whenever one receives subconscious criticism pointed toward the other. As pointed out, the closure of financial markets causes people to remain angry at the government and constantly bash politics publicly. With a thought, the all-terrain Lee super Oscar potential of two people at once stepping down, there would be a slight energy release from the second leading markets. Markets are less physically cap-sensitive; the evolution of the financing paradigm quite simplifies the reason behind this.

I’d like you to please follow the links to learn more about Ex AI subscription pricing for SuperGrog and X Premium. You can also view their API package directly at the GCA forums, which will post all marketed updates as soon as they become available.

https://www.youtube.com/watch?v=Q61fLCh_LZA&list=RDNSQ61fLCh_LZA&start_radio=1

-

Elon Musk and President Donald Trump had a bromance closer than any two individuals can have. However, as time passed, the relationship deteriorated until last week when Elon Musk went postal. There are very close moments in any relationship, and other times when people do not get along. This happens in personal, business, and public relationships. For example, my husband and I were together for thirty years. However, we separated half a dozen times, but eventually got back together. When we separated, it was like we would never get back together again. However, that was not the case. Employees and subcontractors are the same way. There are warm and cold moments. “Elon Musk vs President Trump Feud: Hidden Signs You Missed Body Language Analysis” Elon Musk vs President Trump Feud: Hidden Signs You Missed Body Language Analysis. Watch the video below.

https://www.youtube.com/watch?v=iWvFAKkt2pU

-

This discussion was modified 9 months, 1 week ago by

Lisa Jones.

Lisa Jones.

-

This discussion was modified 9 months, 1 week ago by

-

When people first saw this man walking his pack of six German shepherds without any leashes, they couldn’t believe what they were seeing. The blind obedience the dogs showed left everyone amazed. Some even thought maybe he had forced the dogs into acting this way, but when the truth finally came out, it shocked and amazed everyone even more.

-