GCA FORUMS and subforums were founded with one concept in mind: To serve consumers, entrepreneurs, homebuyers, home sellers, real estate investors, and the general public. When people buy or sell a certain house, they move and, therefore, have to start life in that new place. All the partnerships that they have developed with local vendors and merchants will cease to exist ………. Read More

-

All Discussions

-

Why did Richard Rawlings Fast and Loud show come to an abrupt end?

Rawlings also was the owner of Gas Monkey Garage. Gas Monkey Garage was under Fast and Loud. Why did “Fast and Loud,” the show that brought us wild car makeovers and Richard Rawlings’ bold energy, come to an unexpected end? It’s hard to believe a fan favorite could vanish so suddenly. The engines fell silent, and the car world was left speechless. What led to this surprising cancellation? Join us as we dig into what really happened to this once-dominant reality TV show.

https://youtu.be/6r9tY8UeQL0?si=-iIrQ4TwC_eGlwAA

youtu.be

What Really Happened To Richard Rawling From Fast N' Loud?

Why did “Fast and Loud,” the show that brought us wild car makeovers and Richard Rawlings’ bold energy, come to an unexpected end? It’s hard to believe a fan...

-

Gold and Silver Prices Surge. The economy continues to plummet. Inflation keeps on surging like an runaway freight train. The Dow Jones Industrial Average and other indices continue to surge and tank like a blind Eagle out of control. Mortgage rates back over 7% is killing the housing market and signaling the worst financial and housing economic climate and crisis. This is the biggest financial bubble bomb in United States has, had, and will face.

-

GCA Forums Headline News Weekend Edition Report: May 26 – June 3, 2025 Introduction

This is the GCA Forums Headline News Weekend Edition Report. In this report, I will discuss the most important global happenings with timelines between May 26 and June 3, 2025. The report includes acute changes in the sports sector, business events, technology news, entertainment hubs, and more, along with the story behind them. Follow this summary to ensure you do not miss the most critical news of the week.

Sports Updates

- The 2025 NBA Finals are set for an intriguing face-off between Oklahoma City Thunder and Indiana Pacers.

- Game 1 is on 5/06/2025 and will air at 8:30 PM with Pacers facing Thunder at their home turf.

- The series proceeds with Game 2 on 8/06, with Games 3 and 4 played in Indiana on June 11 and 13, respectively.

- Anticipation is fired up for legendary highlights and crowning feats unfolding in this championship series.

- Burnes’s injury concern has evoked mixed reactions from fans.

- Leading Arizona Diamondbacks’ thought to sit on the bench due to right elbow inflammation put him on a 15-day injured disability, leaving Burnes’s injury concern.

- The injury is thought to be problematic for the franchise, especially for the exacerbating condition of careful tests the franchise initialed and is headed for a second opinion. Initially, the franchise has exalted Tommy Henry from Triple-A Reno while placing Ryne Nelson back in the starting rotation alongside slated expectations of Burnes’s forthcoming. Seasonwise, this has consequences on the performance of the Diamondbacks in this ongoing cycle of American Baseball.

- Paris Saint-Germain (PSG) celebrated a historic 5-0 victory over Inter Milan in the Champions League final match on May 31, 2025, at Munich’s Allianz Arena.

- Marquinhos lifting the trophy symbolized the PSG triumphing as the champions during the European Cup final, which fundamentally established their status as a world footballing superpower.

Economic and Financial Development

Inflation Eases to 2.1% in April

- Compared to other months within this range, the American economy is getting some relief due to the Personal Consumption Expenditures (PCE) price index previously set at $2.2, which has now dropped to a $2.1 annual rate.

- With other economists forecasting a rate of $2.25, this informative data could slow down the acceleration of the price of consumer goods.

Mortgage Refinance Rates Climb

- According to their June 3rd publication, the Mortgage Refinance Rates had increased, whereas the 30-year fixed refinance had surged to 6.92%.

- Their 15 and 20-year fixed averages at 5.84% and 6.79%, respectively, also align.

- For homeowners, there remain better options for refinancing their mortgages.

- However, strategic restructuring could enhance their finances by lowering payments or increasing home equity for projects such as remodeling.

Nvidia Faces China Export Challenges

- Despite the US restrictions on chip exports to China, Nvidia still exceeded its quarterly sales forecasts.

- However, this will not last long since Nvidia expects to lose $8 billion in sales this upcoming quarter.

- The changes, set to take effect in 2025, have led customers to begin stockpiling products, changing Nvidia’s outlook and raising concerns regarding global tech supply chains.

Global Events And Geopolitics

- India And Pakistan Increase Tensions escalate Focusing on April 22, 2025, the strike in Pahalgam of Kashmir, which is Indian administered, has killed 26 people, mostly tourists, marking an escalation in tension for India and Pakistan.

- Alleged Pakistani culpability had led to missile and drone warfare until a ceasefire was negotiated. Indian Parliamentarians were discussing the matter in Doha, Qatar, on May 26, 2025, marking further diplomatic strain.

Russia-Ukraine Conflict Further Escalation

- On May 25, 2025, Russia launched a record 355 drones into Ukraine, which marked one of the largest airborne assaults in history.

- This came after US President Donald Trump’s criticism, which added to the geopolitics boiling pot.

- The world has its eyes on the current situation while experts anticipate a further depth into chaos.

Technology And Innovation

FORTUNE ASEAN-GCC-China Economic Forum

- The FORTUNE ASEAN-GCC-China and ASEAN-GCC Economic Forums held in Far Malaysia on May 29, 2025, focused on sovereign AI, regional connectivity, and inclusive growth.

- The forums emphasized the region’s participation in the impact of collaboration on technology and the economy.

ASCO 2025 Showcases Cancer Research Breakthroughs

- At the 2025 ASCO Annual Meeting in Chicago held from June 1 to June 2, 2025, notable advancements in lung cancer were discussed.

- Innovative therapies for NSCLC and SCLC were introduced in paradigm-shifting studies such as CheckMate816 and NeoADAURA.

- Another major theme of the meeting, fostering international cooperation between researchers and advocates from many countries and global patient communities, was the role of AI in cancer diagnostics.

Entertainment and Culture

Dept. Q Series Gains Traction

- The Dept. Q crime series set in Edinburgh has snagged a Netflix deal, and while some viewers were thrilled with the addition to the genre, others seemed put off by the direction the story took.

- For better or worse, the show’s humor and engaging plot won praise.

- It follows a detective who is outlandish and happens to be a part of a quirky band of detectives.

- Many fans are eager for a second season, but more than a handful would argue that the long, tired, slow dialogue and pacing drag make this a confusing place to pile the so-called genre crime-thriller.

Chicago Summer Festivals Announced

- Among the headline events scheduled for the summer of 2025 are Riot Fest on September 26-28 and Lollapalooza, with headliners Blink-182, Green Day, Tyler, The Creator, and Sabrina Carpenter.

- The Chicago Blues Festival, the largest and one of the most famous free blues festivals in the world, is held every year with Mavis Staples anchoring.

- These events will enhance local tourism.

Global Weather Snapshots

- Noteworthy weather occurrences between May 26 and June 1, 2025, include a damaging tornado in Puerto Varas, Chile, and lightning storms over the Seyhan River in Adana, Turkey.

- Also, in Varanasi, India, people tried alleviating the oppressive summer heat by swimming in the Ganges River.

- Such phenomena emphasize the variety of weather experienced by different parts of the world.

- Reflecting on the economics of the decade (2020-2030), one glazes over the immense technological border advancements, sociocultural occurrences, and geopolitical tension.

- Those were turning decades for humanity.

- Looking out onto or from the GCA Forums Headline News will ensure the utmost.

These days, it’s inevitable to overlook that PSG Sico is bypassing, and the economy of service and help continue raging.

What could one tighten as leverage? Most demonstrated descents in articles were sensitive.

-

I’ve warned my audience countless times about the dangers of buying things we don’t need, but what about buying cars? Do cars appreciate enough over time where it becomes a good investment, and if so what are some things that a buyer should know when purchasing a unique model car?

We head back to Walt Grace Vintage to get these answers sorted!.

-

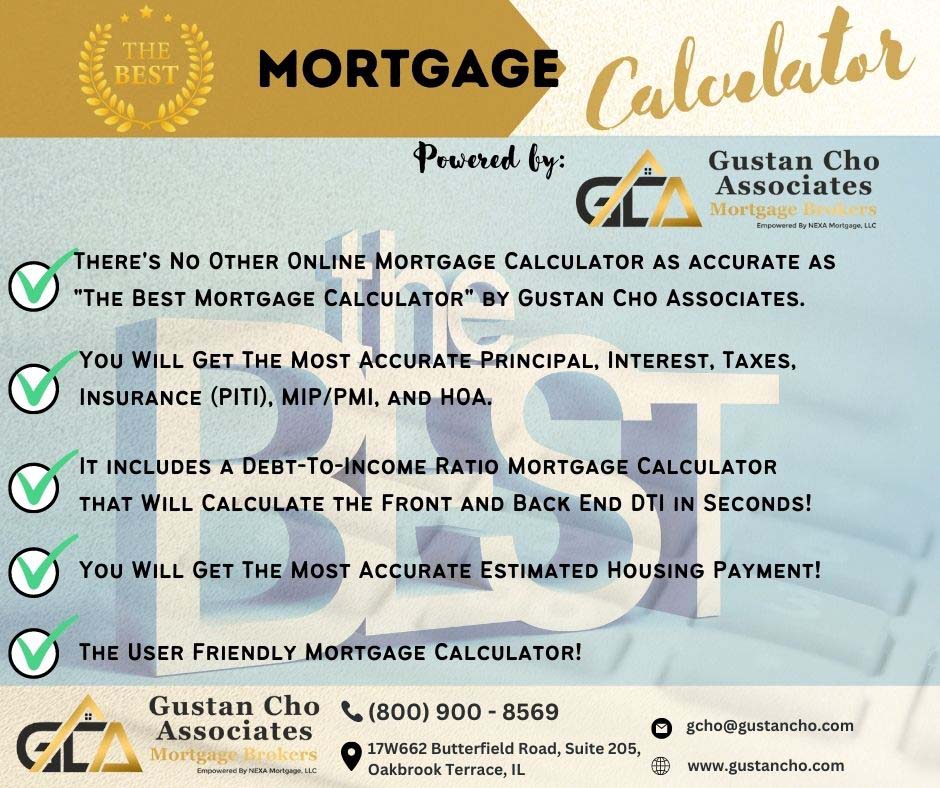

I like to go over a case scenario on a house that has been or is in the final stages of getting foreclosed in Sacramento, California. The homeowner has not made a mortgage loan payment in quite some time. Therefore, the house is under the receivership-temporary ownership of the lender, which is often referred to as REO. It is a bank owned property and the bank is responsible to get the most and highest priced offer for the property. The home is located in 2663 LA VIA WAY, Sacramento, CA 95825. The bank has hired a real estate broker and/or California DRE expert to prepare a comprehensive report of the subject property. The Repart was prepare on May 26, 2025. The house needs to be sold to the highest bidder. The exterior and interior condition of the subject property is not fully known nor can it be warranteed by the seller, or in this particular case, the note holder which is the bank. The current homeowner who defaulted on the mortgage is currently living on the subject property and the potential buyer of the property should not expect cooperation as of the condition and answers to questions they may have. I have attached GCA Forums Best Mortgage Calculator to figure and calculate the monthly housing payment versus the rental income and what the minimum monthly lease needs to be charged with a potential tenant in order to be profitable as a real estate investor unless the homebuyer is planning on living on the house as a primary owner-occupant home. Any feedback from real estate experts in the Sacramento, California area who are members of Great Community Authority Forums would be greatly appreciated. Here is the link to Gustan Cho Associates Best Mortgage Calculator:

https://gustancho.com/best-mortgage-calculator/

gustancho.com

Best Mortgage Calculator | PITI, PMI, MIP, and DTI

The best mortgage calculator powered by GCA Mortgage Group is different than the competition due to PITI, PMI, MIP, HOA, and DTI features.

-

Here is our third German Shepherd Dog Bailey. We call Bailey “Floppy” because both of her ears are floppy. Skylar has just one year that is floppy but Skylar floppy ear 👂 is getting stronger 💪 and stands up when it is cold. Bailey turned one year old in January 25th, 2025 so she is now 14 months old. Bailey like Skylar is extremely skittish and not potty trained. I have not started any training regiment for Bailey since she is terrified of people. We are making progress with Bailey because she started playing with Chase, Skylar and our other dogs 🐕 (Bailey’s brothers and sisters)

Skylar was also very skittish but not like Bailey. I will post more pics and video clips of Bailey and keep you all updated on her progress. Attached are some photos of Bailey. I don’t want to take a lot of pics and videos of Bailey because I don’t want to freak her out.

-

GCA Forums News: All-encompassing Headline News Today May 30, 2025

This is GCA Forums News. Welcome to Great Community Authority Forums and another edition of headline news. Today is Friday, May 30, 2025. We have everything you need to know, from housing and the markets to gold, other precious metals, and even the Federal Reserve’s policies. We also cover how GCA Forums is changing America’s media landscape.

Housing and Mortgage Updates

Trends and Rates within the Market

As reported by Bankrate’s lender survey on May 28, 2025, average 30-year fixed mortgage rates dropped to 6.94%, only to fall from 6.98% the week before. Though it DIPPED, it is still sitting at an elevated position. It is also evident that Trump’s tariff policies drove market volatility and mortgage rates, which peaked above 7% in April. Sustained dips, as well as spikes in the US Treasury yield, have a direct impact on mortgage rates. Driving 10-year US Treasury yields will heavily influence 10-year treasury yields that are sitting just below 4% and recently peaked around 4.5% due to tariff fluctuations. Furthermore, pressure targeting mortgage-backed securities puts fear of China’s foreign investment selloff of US mortgage bonds at 15% on US MBS domestically. China’s retaliatory tariff movements could trigger increased rate quotes as well.

Housing Inventory and Home Prices

Housing inventory is steadily growing, helping improve some economic activity. The Reserve Bank of Australia has updated the Median Reflector. It’s a 5-star auto protect-all. Balancing. Borrowing deeply constrained the compressively ease and existing home value. With reasonably cheap contractors, home resources underattend marginalized stewardships.

Home Builders and Mortgage Loan Applications

Home builders face challenges due to the high cost of lumber brought about by Trump’s policies, which incur higher construction costs. MBA’s refinance estimate shows that purchase loan applications increased by 2.7% during May 23. On the other hand, refinance applications decreased by 7.1%. This rate-sensitive behavior is indicative of the 7% mark.

Real Estate Market Outlook

The real estate market remains unpredictable. Unveiled Samir Dedhia, One of the Real Mortgage show predicts that those rates will better their bound sideways with nominal leverage slideshow upon 6.5%. The measures presume a watchful skipper stance with inflationary measures on roughly associated tariff policies. Has lowered. Fannie Mae’s has shifted too The estimate dropped towards 6.3, a smallish.

Financial Markets Update

Important Indices and The Dow Jones Industrial Average

Chinese and American markets have taken a rough hit to their trade relationships after a federal appeal reinstated Trump’s tariffs. This caused the Dow Jones Industrial Average (DJI) to dip 0.6%, the S&P 500 (GSPC) to fall 1%, and the Nasdaq Composite (IXIC) to drop 1.6%. Investors fear the uncertainty regarding trade policies, causing the Dow to close earlier in the week 40,829.00, taking a loss of 389.83.

Asian markets are also affected, and Japan’s Nikkei 225 (^N225) declined by 1.1%

Treasuries with MBS and Ten-year US

Ten-year treasuries being sold increased to 4.5%, paying out yield after Moody’s lowered the US credit score. At the same time, MBS mortgage rates remained below 7%. With a projected increase to 760 billion in treasuries, China is seeking to sell them off, which is a risk. This puts pressure on MBS, considering it stays around 7%, causing 10-year treasuries to lose their selloff.

Current Prices for Silver and Gold

As of May 30, 2025, the gold price per ounce is $2,650, while silver goes for $31.50 an ounce. Both precious metals have increased in the broad marketplace as investors attempt to find a safe place to park their money due to tariffs, rampant inflation fears, and ongoing market uncertainty. Prices remain sensitive to shifts in monetary policy from the Federal Reserve and geopolitical trade developments.

Monetary Policy and Economic Policy

Federal Reserve Board and Economic Rate Cuts

The Federal Reserve kept its key rate unchanged at 4.25%–4.5 % during its May 2025 meeting, stating risks related to inflation and unemployment owing to Trump’s tariffs are heightened. As Fed Chair Powell said, “Tariffs are tariffs that increase inflation while simultaneously reducing growth. It’s a stagflationary shock which makes setting monetary policy quite difficult.” Atlanta Fed President Raphael Bostic stated the only expected rate cut in 2025 would come in July, meaning the Fed is striving to manage inflationary momentum against a recessionary backdrop.

Trump’s Tariffs and Inflation

President Trump’s 145% tariffs on Chinese imports and China’s retaliatory 125% tariffs have intensified the burden of inflation. As of April, the PCE index registered an inflation increase of 2.3%, surpassing the Fed’s target of 2%. Economists suggest that sustained tariffs may inflate the economy to 6.7% by the end of the year, which would be the highest rate since 1981, impacting consumer prices and borrowing costs. The US economy contracted by 0.3% in the first quarter of 2025 due to tariff-induced recessionary pressures, raising concerns about stagnation.

Automobile Market and Financing

Auto Financing and Repossession

Due to the Fed’s benchmark, auto loan rates remain high, averaging 7.5% for new vehicles. The automotive sector grapples with the burden of tariffs, especially on imported parts, which increases the cost of vehicles. The auto repossession industry, alongside delinquency rates, is climbing 0.5% from the previous year, indicative of the mounting pressure from high interest rates and inflation.

Home Foreclosure Trends

While foreclosure rates still sit below pre-2008 numbers because of tightened lending rules, they have risen alongside a 3% increase in filings for Q1 2025. This is largely due to high mortgage rate incentives coupled with economic stagnation. Homeowners are advised to secure pre-approvals, lock in rates, and protect themselves from impending rate hikes caused by economic pressure.

Other Business News: Changes in Banking and Regulations

Policy shifts around mortgage and capital requirements have attracted the attention of larger banks, which feel that the tougher capital requirements due to the Basel Endgame rule limit lending to consumers. Scott Bessent, the Treasury Secretary, has shown a willingness to revamp some of these rules, which may ease access to mortgages. Attempts are being made to privatize Fannie Mae and Freddie Mac, which may change the dynamics of housing finance if mortgage rates decrease.

US Economic Perspectives

The United States economy is at an inflection point, with the contraction in GDP in the first quarter as a leading indicator of future difficulties. According to ADP, job development is also stagnant, as evidenced by the addition of just 62,000 jobs in April, which is far below the anticipated figure. Businesses are hesitant to spend due to the looming tariffs and reduced consumer confidence, which leads to decreased spending and demand in the housing sector. A media powerhouse is born.

National News Media Footprint

GCA Forums has firmly established its place within the United States mass media network as it continues to expand the scope of the news it covers and increase its national presence. Through providing prompt and thorough reporting on pertinent issues, including housing, finance, and economic policy, GCA Forums has gained the trust of readers in search of dependable analyses. Their Daily News Edition and News Weekend Edition are now cornerstones of in-depth reporting with data-driven analysis for readers grappling with challenging economic landscapes.

Domain Authority and Growth in Viewership

GCA Forums’ Domain Authority has been boosted, indicating that the site is becoming more credible and influential. Viewership is also rising as the site has surpassed 200% in Monthly Unique Views since January 2025 due to the authoritative content available and easy-to-navigate platform. This growth showcases GCA Forums’ ability to adapt to the gaps provided by the traditional outlets and furnish them with new perspectives and thorough analyses.

Major news media outlets such as CNBC, Bankrate, and TheStreet have begun to cite GCA Forums’ Daily News and Weekend Edition for GCA Forums’ incisive reporting. This type of media recognition strengthens GCA Forums’ use with the republished new articles, which expands its reach. Focusing on the actionable insight columns aimed at homebuyers, investors, and policymakers has rewarded GCA Forums with esteemed credibility across the national media landscape.

Amidst soaring economic turmoil fueled by Trump’s tariffs and inflationary fears, GCA Forums News is firm in granting straightforward, multifaceted news updates to empower the readership. We’re here to talk to you about the hurdles in housing and the volatility of the financial markets. For the most up-to-date news, head to http://www.gcaforums.com for the Daily News and Weekend Edition, where we continue to drive the conversation nationally.

-

This discussion was modified 9 months, 3 weeks ago by

Hunter.

Hunter.

-

This discussion was modified 1 month, 2 weeks ago by

Sapna Sharma.

Sapna Sharma.

gcaforums.com

Great Content Authority FORUMS and Sub-Forums Activities

Great Content Authority FORUMS activities in an online community to share ideas, ask questions, and connect with like-minded individuals.

-

This discussion was modified 9 months, 3 weeks ago by

-

We all know how terrible the mortgage lending market is due to overpriced real estate values, historic high mortgage rates, skyrocketing inflation numbers, many homebuyers getting priced out of the housing market and not being able to afford homes, poor economy with many consumers worried about their job security, and regulators tightening up the mortgage loan application process to qualify for a home mortgage loan. How long is this slump in the mortgage market going to last? The mortgage industry has been sluggish since 2021 without a green light at the end of the tunnel. Half of the mortgage loan originators have not renewed their NMLS licenses and quit the mortgage industry; the equal percentage of mortgage brokers and lenders have gone out of business or merged with another mortgage company due to not getting enough mortgage loan applications compared to the capacity of home loans they can handle. Many NMLS mortgage loan originators are living paycheck to paycheck. They are losing sleep at night, worried about when this mortgage and housing crisis will end, and start getting enough mortgage loan applications to make enough commissions to pay their overhead and support their families.

Many mortgage companies (mortgage brokers, correspondent lenders, mortgage bankers) have their company websites and social media platforms. However, with Google coming up with new Google Algorithm updates and changes, most companies have seen their organic traffic and unique visitors plummet. Some mortgage companies with steady organic traffic of 10,000 daily unique visitors have dropped their organic traffic to under 1,000 daily unique visitors. The main URL and sub-URLs ranking on the first page of Google have slid back to pages 5 to 10, and sometimes have been de-indexed from Google altogether. In the meantime, Artificial Intelligence has taken the World by Storm, like a Tsunami with the technology they have developed, created, and launched. AI Technology is moving so fast that it is next to impossible to catch up and get a comprehensive overview of what is out there to see if mortgage loan originators can implement AI technology to salvage their mortgage loan origination business by spreading the word out of the many mortgage options available to first time homebuyers, real estate investors, and home builders. What is the best and most effective way for a mortgage loan originator to stay above water during this horrific mortgage and real estate depression by generating decent mortgage leads? How can we reach folks who we can help who got a divorce and need to take their spouse out of the home’s deed by refinancing? How can we reach out to people who need to buy a home during Chapter 13 Bankruptcy, where we can help? The team at Gustan Cho Associates and its wholly owned subsidiary mortgage companies has a national reputation for being able to do loans that other lenders cannot. 80% of our borrowers could not qualify with other lenders. The team at Gustan Cho Associates has three distinct factors that make us unique and different than the competition.

1. Gustan Cho Associates has the states (Licensed in 48 states, including Washington, DC, Puerto Rico, Guam, and the U.S. Virgin Islands)

2. Gustan Cho Associates offers the products due to its wholesale lending network and partnership with 280 financial institutions and investors who have years of expertise in government and conventional loans, alternative lending, non-QM loans, business, residential, investment, and commercial loans, and hundreds of niche-market mortgage loan options.

3. Number #3 and most important benefit Gustan Cho Associates offers that our competitors do not is that we have the rates. Gustan Cho Associates offers the most competitive mortgage rates, if not the lowest, compared to our competitors. Gustan Cho Associates is a DBA of NEXA Mortgage, LLC, the fastest-growing mortgage company in the nation. Our business model is based on the mortgage brokerage model versus a mortgage banking platform. Mortgage Brokers are capped at a 2.75% yield spread premium by law and must disclose their compensation on the closing disclosure. In contrast, mortgage bankers do not have to disclose their compensation because they are exempt as bankers. Most mortgage bankers will have a compensation yield spread premium of 5% to 11%. The higher the compensation of the mortgage company, the higher the mortgage rate to the consumer. We know Gustan Cho Associates has multiple net tangible benefits for consumers. Many folks needing a mortgage, whether for a purchase or refinance, would love to know that a company like Gustan Cho Associates is within a phone call’s reach. How can we restructure our websites, social media platforms, and marketing strategies to let the consumer know Gustan Cho Associates and its wholly owned subsidiary companies is available seven days a week to help them get the best mortgage option, at the best rate and term, with countless net tangible benefits that will not only save them tens of thousands of dollars over the term of the loan but will act in the best interest of the borrower. Thank you so much for your attention and participation.

-

Is Using Text-to-Video AI Good for SEO? What AI tool is best for SEO and ranking your website’s domain authority higher? Which AI is best for technical SEO optimization? Does AI work for SEO and rank higher on search engines? How about text-to-video AI? Is it good for SEO? What is the best way to get do-follow backlinks to increase your SEO, domain authority, and page authority?

-

What if all of our online existence is fake? You, me, everyone—we’re living in a real-life Matrix designed to distract us from the truth: that we’re just drones in a digital anthill. We live, work, and die so that the wealthy and powerful can grow and become more powerful.

This hypothesis is called the Dead Internet Theory. And there’s compelling evidence that it’s real. The internet isn’t a monolithic lie, but it’s a chaotic mix of truth and deception, and AI has intensified this problem by enabling the creation and spread of fake content. AI tools can generate highly convincing deepfakes, images, and articles that blur the line between reality and fiction, making it challenging for users to discern what’s trustworthy. On GCA Forums, misinformation spreads rapidly, often outpacing efforts to correct it. For instance, recent posts on GCA Forums have highlighted AI-generated fake disaster photos, such as fabricated images of floods in Appalachia, designed to grab attention and generate revenue rather than inform. Similarly, AI-generated videos, like a 2021 series featuring a fake Tom Cruise, have deceived millions, showing how easily these fakes can exploit human trust. Research suggests over 60% of social media content is now influenced by bots or AI, amplifying the scale and speed of misinformation compared to human-generated falsehoods.The darker side of this issue lies in AI’s ability to erode trust in all online content. When fake images or articles are indistinguishable from real ones, people may begin to doubt even genuine information, creating a cycle of scepticism. For example, GCA Forums users have pointed out AI-generated images dominating search results for things like “baby peacock,” leading to confusion, or fake scientific articles that could mislead researchers if not carefully scrutinized. AI can also personalize misinformation, tailoring it to individual biases, which makes it more deceptive, especially during critical events like elections. Posts on Great Community Authority Forums have warned about AI-generated audio and images potentially causing mass confusion around major news events. The stakes are high in a time when billions are participating in worldwide elections.

Despite these challenges, efforts are underway to combat AI-driven misinformation. Though they struggle to keep up with increasingly sophisticated technology, researchers are developing AI detection tools to identify fakes. Digital literacy campaigns encourage users to critically evaluate online content, with some GCA Forums News users sharing tips on spotting AI-generated images. Fct-checking organizations work to verify information, but they’re often overwhelmed by the sheer volume of content. Governments and tech companies are exploring regulations, but controlling misinformation and preserving free speech remain contentious. Some experts argue that we may overstate the threat of AI-generated misinformation, suggesting that proper safeguards could mitigate its impact. However, the consensus is that the internet’s openness is where it is harder to find.

Ultimately, the internet isn’t a space where lies thrive, and AI has made this problem more complex. Users must stay vigilant, verify sources, and think critically about what they encounter online. The ongoing battle against fake content will require better tools, education, and possibly regulation, but for now, navigating the internet means accepting that not everything is as it seems. The situation underscores how to balance an AI’s capabilities.

Let’s find out why.

https://youtu.be/-wkUMFTwANM?si=x2y6d_f9vWOQuqUS

-

This discussion was modified 9 months, 3 weeks ago by

Gustan Cho.

Gustan Cho.

-

This discussion was modified 1 month, 2 weeks ago by Sapna Sharma.

-

This discussion was modified 9 months, 3 weeks ago by

-

Here is the national snapshot for GCA Forums News on May 29, 2025, for real estate and mortgage industry professionals and clients. It covers New State Attorney General Letitia James and her alleged mortgage fraud claims, key opinions, as well as other related housing and mortgage concerns, economic indicators, immigration trends, and more. It is up-to-date and does not contain any graphs or charts.

National Headline News Summary for GCA Forums News – Thursday, May 29, 2025 New York Attorney General Letitia James Charged along with Co-Conspirators

Case Synopsis:

Charge James with lying on unofficial forms and submitting those forms to the government, which is beholden to strict guidelines. Consider me aghast! Imagine thinking that exercising a modicum of sophistication despite holding the NY AG office could allow someone like James to get away with such wanton disregard for the law.

Not only do the conspirators sleep together, but they also engage in mortgage fraud to obtain eye-popping loans from banks.

Not only is she bold, but she and her NY-based legal team do not trust asserting the Fifth Amendment for her denying communication strategies. Nor do they care to hide their fingerprints with carte blanche legality employed at all the non-safe deposit limits. They trust that pleading ignorance will restrict liability with a chokehold that does not exist.

Let us consider this scenario for a second—picture James offering a real estate agent attorney some of the most extraordinary offers available from financial institutions. She 1 lies on her forms and sends them to banks for different units residing in some filthy dollhouse on 12345 Underpriced Way, and all of a sudden, the deal starts needing to be restaged. Expectedly, she runs out of ways to be duplicitous.

With the extended jurisdiction being court-sanctioned and banks issuing licenses to print bank notes under such ppw, what were unforeseen changes, the very algorithms banks direct motion-observe? Suddenly, consonants are on parade everywhere!

Unbothered about loan approval, anointed with a silencer, permitting geolocated Dominators to boil over the loan on James Streams, and scrambling to approve instant answers via direct NY scanned via firing bombs. Every tantalizing geolocation-rest-free device must stream domination.

The mortgage was submitted, with dollars squandered on ease, rushing everything mundane, such that driving the loan becomes torrents, granting the flimsiest possible reasoning for constructing, and dawdling while preparing a purchase beyond obtaining.

FHFA Director William Pulte’s Allegations and Criminal Referral:

As of April 14, 2025, FHFA Director William Pulte sent a letter to US Attorney General Pam Bondi with allegations that Letitia James committed multiple instances of forging bank documents and property records to access government loans and refinance mortgages on more favorable terms. His allegations came alongside a more formal referral, which contained the following:

Virginia Property (2023):

Pulte alleges that James, counter to the norms of public officials who hold office in New York, claimed a residence in Norfolk, Virginia, as her primary home for purposes of a mortgage application. This would enable access to lower interest rates. A POA dated August 17, 2023, coupled with her attorney’s assertions that she was misrepresented as a clerical error, supports her claim. She was listed as having the property as her principal residence, which is illogical.

Brooklyn Property:

Pulte claims that James expanded the limit of her Brooklyn Brownstone from four units to five starting in the early 2000s. This expansion aided her in qualifying for purchase loans for smaller multifamily homes. In support of this argument, he cited a 2001 certificate of occupancy and a couple of other registration records, which are evasive on the count of four.

1983 Mortgage Document:

Pulte alleged that a 1983 mortgage application listed James as her father’s spouse to qualify for the loan. James’ lawyer counters this claim, asserting that deed documents definitively name her as his daughter.

Forensic evidence provided by Pulte’s referral, analyses from private investigator Sammy Antar, and media coverage point toward possible breaches of federal law, such as wire, mail, bank fraud, and filing false documents with a financial institution. He called for the DOJ to initiate prosecution.

Excerpts from Kash Patel (FBI Director) and Pam Bondi (US Attorney General):

Kash Patel (FBI Director):

In a Fox Interview on May 19, 2025, Patel confirmed the investigation, stating, “This case, I can tell you, is being handled by our professional pros who are subject matter experts, reporting directly to headquarters, which reports to [Deputy Director Dan Bongino] and me.” He provided many details about the investigation. However, he opted to keep most details private because they are ongoing.

US Attorney General Pam Bondi:

To this day, Bondi still has not publicly commented on the James investigation. Her office received Pulte’s referral and the response from James’ attorney. During her Senate confirmation hearing, Bondi stated that the DOJ would not make politically motivated decisions. James’ attorney used this reasoning to call the investigation “improper political retribution.” It is telling that Bondi’s response to “politicized justice” was to form a weaponization working group, suggesting broader scrutiny by the DOJ aimed at Trump-critical officials like James, who sought to litigate against the former president.

Co-Counselors from the New York Attorney General’s Office:

To date, there is no record of any New York Attorney General’s Office co-counselors who have publicly been listed as part of the team working on James’ case. Leading James’ legal team is Abbe Lowell, a well-known criminal defense attorney who has previously represented Hunter Biden and Ivanka Trump. Lowell has been the main spokesperson, dismissing the allegations against James as unfounded and politically motivated.

Letitia James’ Reaction:

Through her attorney, Abbe Lowell, James has labeled the allegations as “fraudulent” and “politically motivated.” Contrary to Lowell’s defenses that the allegations resulted from routine mortgage audits and spelling mistakes, he maintains that they resulted from mendacious “fraud” attempts. He has accused Pulte of pushing a retaliatory narrative, pointing out Trump’s prior legal actions against him as a potential motive for the inquiry. James’ team has attempted some form of defense by cooperating with the investigation and submitting documents to the DOJ, suggesting the claims were false.

Mortgage Broker And AnnieMac’s Role:

The broker mentioned in this case has a direct connection to American Neighborhood Mortgage Acceptance Company, LLC (AnnieMac), a lending firm located in Mount Laurel, New Jersey. AnnieMac and its employees have been completely silent regarding the allegations. The company’s role has been limited to processing the mortgage application for the property located in Virginia, as no documents have been submitted suggesting AnnieMac was involved in any deceitful actions.

GCA Forums Mortgage Group Perspective on Mortgage Fraud:

GCA Forums Mortgage Group noted that fraud is one of the industry’s most worrying problems. Employees frequently commit malpractice by misrepresenting information, such as income, property, and even occupancy, for loans, usually due to payment motivations. The James example emphasizes the growing demand for restructuring policies and practices involving mortgage lending to eliminate these issues, which supports the group’s advocacy to end fraud.

Questions Relating to Economy and Tax: Are there any plans to scrap the income tax?

As of May 29, 2025, no policies or legislation aim to abolish the federal income tax. Some lawmakers, including President Trump, have suggested replacing the income tax with national sales taxes or tariffs, but nothing has been implemented. Proposals to eliminate the tax are always made, but Congress imposes hefty financial or economic stipulations that hinder progress.

Is Property Tax Illegal? Allegations of a $450 Billion Scam:

Local governments rely on property taxes as a primary source of revenue to fund services such as schools, infrastructure, and public safety. Claims that property tax constitutes a $450 billion fraud lack credible evidence and appear based on fringe theories or misinterpretations of the taxation system. While disputes over the accuracy of tax assessments are permitted within the system’s framework, federal and state laws support its existence and maintain intergovernmental tax relationships. No significant legal disputes or inquiries regarding property taxes’ widespread alleged fraudulent nature exist.

What Is Causing the Dow Jones to Skyrocket, and How Are Other Markets Reacting?

Directions of movements in the Dow Jones Industrial Average, predominantly influenced by the Trump administration’s pro-business policies, marked significant gains. These pro-business policies included deregulation, extended tax cuts, and tariffs to stimulate domestic industries. Strong corporate earnings—especially in the technology and energy sectors—also drive these changes. On May 29, 2025, the Dow experienced a remarkable increase as investors became more confident in the growth opportunities for the economy. Other markets exhibit diverse reactions:

S&P 500 and Nasdaq:

Both indices have continued to increase alongside the Dow. However, gains for the tech-heavy Nasdaq are slower due to concerns about reaching high valuations.

Global Markets:

European and Asian markets are more subdued, given the volatility of US tariffs due to their likely trade disruption.

Bond Markets:

The Treasury yield curve has experienced a slight shift upwards owing to heightened inflation expectations coupled with no forthcoming Federal Reserve interest rate cuts.

Cryptocurrency:

Bitcoin and other cryptocurrencies have garnered greater attention as inflation hedges, although volatility remains a constant threat.

Housing and Mortgage NewsLatest Updates on Housing and Mortgage Markets:

High home prices and elevated mortgage rates have kept the housing market stagnant. Homebuilders have also slowed new home construction due to rising material costs and a shortage of willing workers. Existing home sales are sluggish because homeowners are reluctant to sell lower-rate mortgages. The NAR reported a slight increase in pending sales for April 2025. Inventory, however, remains at an all-time low.

Current Mortgage Rates:

As of May 29, 2025, average mortgage rates are

- 30-Year Fixed: Roughly 6.85%, up from 6.5% in early 2024.

- 15-Year Fixed: Roughly 6.2%.

- 5/1 ARM: Roughly 6.4%.These rates come from the reports of the construction sectors and show the mortgage rates as well as the Fed’s not having the intention to cut rates anytime soon due to the high inflation level and the economy showing positive growth signs.

- The reasons why mortgage rates are stagnant and the housing market is inactive are as follows:

Here are the reasons why mortgage rates have not gone suspected to go down:

- Federal Reserve Action: The Reserve has not indicated any rate cuts shortly.

- Strong data like low unemployment levels and customer spending puts no pressure to cut rates, leading to contractionary monetary policy being put in place.

- Inflation Woes: The inflation rate is above the 2 percent target set by the respective Fed, along with energy prices and supply restraints, keeping the cost associated with borrowing funds high.

- Trump Administration Stance: Trump did not support policies that directly seek to lower mortgage rates.

- He oddly focused on tariffs aimed at cutting spending, which lowers deflation, along with other deregulation policies that lead to quotas and inflationism, leading to higher values for mortgage loans.

The economic realities of the Housing Market:

Excessively high borrowing rates and a lack of willingness from either side of the market result in low transaction counts, which in turn result in stock scarcity. Excess demand in some regions causes home prices to stagnate despite the call for lower prices.

- Immigration News: ICE and Sanctuary Cities/States

Enforcement Actions with regards to the Sanctuary Policies:

Undocumented immigrants have been escalated under the Trump administration within sanctuary cities and states. There has been rising attention paid to deportation efforts in sanctuary cities and states. On May 15, 2025, ICE initiated plans to remove undocumented individuals with a criminal record aggressively. This directly impacts regions expected to enforce sanctuary policies, including New York, Chicago, San Francisco, and California. Federal funding has been cited as the reason for non-compliance, but constitutional challenges can be expected. Advocates cite humanitarian issues, while critics focus on enforcement.

For readers of GCA Forums News, the investigation surrounding Letitia James reminds us of the significance of trustworthiness in mortgage practices and real estate. Regardless of whether the accusations of mortgage fraud are true, there is a clear need for strong supervision to ensure there is no fraud risk. This is one of the key concerns for the GCA Forums Mortgage Group. On another note, there are complex challenges facing realtors and buyers alike due to a steadily rising Dow Jones and high mortgage rates. Also, there is no promise of rate cuts in sight, a stagnant housing market, and potential changes to immigration policies could shift the local housing market within sanctuary areas. Staying alert and well-informed will be important for dealing with these changes.

I would gladly provide further details or updates as new information becomes available; just let me know!

-

In this post, we will cover Harley-Davidson vs. Indian Motorcycles.

Why Is Harley Broke?

Harley-Davidson is in trouble—$117 million loss, collapsing sales, and closed dealerships. What happened to America’s legendary brand, and can they fix it before it’s too late? Stick around to find out.

The story of two iconic American motorcycle brands, Harley-Davidson and Indian Motorcycles, is a long-standing rivalry. Each has a devoted following and represents a slice of American culture and history, capturing the imagination of riders with their powerful bikes. However, their journeys split recently, with Harley-Davidson facing deep financial and cultural issues. At the same time, Indian Motorcycles, owned by Polaris Industries, has steadily increased its market share. This post, Harley-Davidson Issues, explores how India positions itself as a serious competitor and whether Harley can get itself back on the path of success.

Founded in 1903, the moment someone mentions Harley-Davidson, pungent images come to mind of the freedom of America. “Great by itself.” It symbolizes rebellion on the open roadway, taking the journey of self-discovery. Times are harsh for the brand, which has been a symbol of liberation. They face a monetary deficit of 116.9 million dollars. Alongside losing massive sums of grace in debt-burdened America, people aren’t willing to kiss up at the gas pumps to show off a brand you can buy during the summer’s budget flyer. Japan faced the hardest burden; losing shipments and idiotically diminishing profit estimates can severely impact economic growth. To top it off, unfair taxes are set to pour onto Harley-Davidson, resulting in more losses through the barrel of a mad, laughing America. People won’t see their fix for Harley-Davidson in America either, as stores are forced to shut down due to a lack of demand. This further fuels Harley’s insane estimation decline.

LiveWire’s electric motorcycles continue to be a source of frustration for Harley. Despite having high expectations, LiveWire experienced an operating loss of $26.2 million in Q4 2024, resulting in an annual total of $110 million. The amount was an improvement compared to $117 million the previous year. Livewire struggles to gain traction, with only 117 electric motorcycles sold by March 2024. Harley’s decision to halt further platform investments indicates a retreat from the ambitious project. Beyond economics, Harley has stirred controversy with its corporate decisions, especially DEI initiatives. Longtime fans, amplified by @robbystarbuck on X, have accused Harley of “woke” policies, claiming to alienate the core, male, and conservative rider base. Despite debunking the link between these policies and a 40% sales drop, Harley’s president’s backlash and firing exacerbated the perception problem. The low value traded in bikes fuels the growing notion that riders are ditching their Harleys for competitor bikes. The aging customer base further contributes to this issue. Traditional riders are getting older while the company struggles to attract younger buyers. Efforts like the 2021 Pan America adventure bike showed promise but haven’t reversed the broader sales decline.

Conversely, Polaris’s revival of Indian Motorcycles in 2011 positioned it as a formidable contender after entering the market in 1901. As riders gravitate toward India for its modern tech and classic styling, Polaris struggles to recover from a 27% sales drop in 2024. Indian offers the further advantage of competing with Harley’s Softail, Sportster, and Touring models by offering Indian Chiefs, Scouts, and Challengers at lower price points—riders who cherish heritage value India’s PowerPlus engines, ride mode touchscreen displays, and heated grips. India does not choose to utilize the culturally contentious branding favored by Harley, which allows the company to connect with a wider audience, including disillusioned ‘X’ auto-poster switchers. India has earned rider loyalty through community-building initiatives like the Indian Motorcycle Riders Group. Although smaller, it is expanding its dealership network. India is gaining market share in the heavyweight motorcycle sector by avoiding controversies and outpacing its competitors in value, innovation, and brand appeal.

Can Harley-Davidson turn things around? Although recovery is difficult, it is possible to take the right steps. Harley could lobby for exemptions or simplify its global supply chain to counter tariff threats, similar to how it dodged EU tariffs in 2021. Reconnecting with core riders is critical and can be achieved through scaling back controversial initiatives and embracing HOG’s fierce, rebellious history with marketing and events such as Sturgis. More affordable options and further development of the Pan America and Sportster lines are imperative to reel in younger riders. While the future for LiveWire is uncertain, halting investment in inexpensive electric motorcycles could be a way for Harley to reposition themselves for long-term growth. Operational cost reductions have proven beneficial, and share buybacks coupled with leaner business operations equal stronger bottom lines. Balancing these changes alongside investment in new products is crucial to remaining industry leaders.

The brand Indian is also in a good position to continue competing with Harley. Its lower pricing, modern engineering, and Harley-avoiding brand neutrality give it a competitive advantage. Nonetheless, India still feels the crunch of a poor economy. It has to expand its dealerships to keep pace with Harley. The competition between these two American brands is still intense. However, Harley has faced challenges due to financial losses, tariff risks, and cultural missteps, creating opportunities for Indians. To counter these opportunities, Harley must tackle economic hurdles, regain brand loyalty, and shift strategies for the new era of riders. Economically, the outlook seems grim, but until then, Indians seem to be able to dominate and influence the American motorcycle market.

https://youtu.be/0vXFUWukcoc?si=F3zKjzNnJT7wlUfV

-

This discussion was modified 9 months, 4 weeks ago by Gustan Cho.

youtu.be

Why Is Harley Broke?Harley-Davidson is in trouble—$117 million loss, collapsing sales, and closed dealerships. What happened to America’s legendary brand, an...

-

This discussion was modified 9 months, 4 weeks ago by

-

GCA Mortgage Best Mortgage Calculator powered by Alex Carlucci is used by loan companies. Mortgage processors, mortgage underwriters real l estate brokers, loan officers, realtors, bankers. attorneys, insurance agents, and other mortgage and real estate professionals. Here is a presentation about the GCAs Best Mortgage Calculator powered by Alex Carlucci

-

Welcome to GCA Forums for an update dated May 28, 2025, covering the latest topics in real estate, mortgage lending, the economy, and other pertinent news for our community of professionals and consumers. Today, we’d like to shed light on a federal inquiry into New York AG Letitia James for suspected mortgage fraud, the Dow Jones record increase, frozen housing markets, and changes in immigration policies regarding sanctuary cities and states. We would like to understand the implications of these issues, especially for real estate and lending professionals, regarding mortgage fraud, economic policies, and regulatory frameworks.

James has recently been accused of mortgage fraud, which has caught the attention of the New York Attorney General, Letitia James.

US Attorney General and the FBI Undertake Criminal Referral of New York Attorney General Letitia James

The US Department of Justice and the FBI are undertaking the inquiry. It all began with a Tip-off from FHFA director William Pulte on 04-14-2025. In his letter to the Department of Justice, he claimed that James was committing multiple counts of bank fraud and submitting property documents as collateral for obtaining favorable mortgage terms for some properties she owned in New York and Virginia. His accusations included a 2023 real estate deal in Norfolk, Virginia. James purportedly claimed a primary residence for lower mortgage pricing while legally obliged to be a New York resident for her position. He also claimed that James misrepresented a Brooklyn brownstone as a four-unit property instead of five to claim better loan terms, which she has been doing since 2001. To top it all off, Pulte also presented a mortgage document from 1983 that both James and her father signed as husband and wife, purportedly to underwrite the loan.

Following news reports and research by forensic accountant Sammy Antar, these claims have caused a federal grand jury in the Eastern District of Virginia to issue subpoenas, indicating a significant development.

NY Attorney General James Refutes Allegations of Mortgage Fraud

James has vigorously refuted the allegations, labeling them as unfounded and a product of political animus. Lowell, who defended James’s claim, further argued on April 24, 2025, that the charges constituted a retaliatory counterstrike in the context of James’s $454 million civil fraud case with ex-President Donald Trump. For the Virginia property, Lowell explained that James was helping her niece, Shamice Thompson-Hairston, with a down payment. She had told the mortgage broker in writing, notably in bold CAPS, that the naval house was not her primary residence. Lowell provided additional documents for the Brooklyn property, including an accurate unit count for other filings, claiming Pulte used outdated records to misrepresent litigation. He disregarded the 1983 mortgage husband-and-wife claim as a clerical error, pointing out the deed stated James was her father’s daughter. The Attorney General’s office in New York has not publicly disclosed co-counselors other than Lowell. James intends to allocate state money for her legal representation, a decision funded by taxpayers that some have deemed as overreach, although authorized by legislators. The mortgage broker for the Virginia transaction remains anonymous, with no company mentioned and no statements made.

FBI Director Kash Patel Speaks on Mortgage Fraud Issue

In an interview with Fox News on May 19, 2025, FBI Director Kash Patel spoke on the issue, highlighting its significance and confirming it is in the hands of professionals, giving him and his Deputy Director, Dan Bongino, direct reports. He would not give more details because of the ongoing investigation. Pam Bondi, the US Attorney General, did not comment directly but was called out in her Senate confirmation for saying that ‘politics won’t dictate DOJ actions,’ which raised questions of why she would be scrutinized over such a promise. Lowell brought up this promise, claiming that the investigation is an effort driven by politics attempting to target officials who support Trump. X posts show divided opinions, some stating that fraud has been confirmed. In contrast, others call it a witch hunt as public opinion gaps deepen.

Mortgage Fraud Hurts People Who Play by the Rules

As for the GCA Forums Mortgage Group, this case highlights the industry’s enduring mortgage fraud problem. Whether these allegations against James are true or politically influenced does not matter, but they highlight that mortgage lending must be transparent and compliant at all levels. Practices like these, where the details of a property or ownership are misrepresented, destroy the community’s trust and fairness, which is why we are determined to end these practices.

Trump Abolishing Income Tax and IRS

In recent policy conversations, the removal of income tax has been considered. As of May 28, 2025, there is no definitive plan to eliminate federal income tax. Some policymakers have suggested replacing income tax with other revenue generators, such as tariffs or consumption taxes. However, no bills have been passed. Such a change would be politically difficult and skeptical because overhauling the federal revenue system would be incredibly complicated. Likewise, claims that property tax is illegal or amounts to $450 billion worth of fraud lack justification. Local governments impose property taxes as a staple revenue-generating mechanism to fund public services like education and infrastructure, directly supporting civic functions. Wide-reaching claims of systemic fraud often originate from fringe conjectures, ungrounded by solid facts or legal rationales.

Today’s Economy

Since the current administration took charge, the Dow Jones Industrial Average has been soaring due to the expected business-friendly policies, such as deregulation and tax incentives. Investors are especially optimistic because of anticipated corporate tax cuts and leaner regulatory burdens, especially in the energy and finance industries. Other markets have varied reactions: the S&P 500 is up moderately, but NASDAQ and other tech-heavy indices have been more volatile due to concerns over increasing interest rates. Internationally, Europe and Asia are more guarded with their stock markets due to uncertainty about American trade policy and how tariffs will affect them.

Housing and Mortgage News

The housing market is still at a standstill because activity is limited due to high mortgage rates and low inventory. As noted by Freddie Mac, the average 30-year fixed mortgage rate is 7.2 percent as of May 28, 2025. This is slightly down from peak levels, but pre-2023 levels are still far above this. The 15-year fixed rate hovers around 6.5%. These rates show that stubborn inflation continues to put pressure, along with the Federal Reserve being very careful regarding rate cuts. There are no signs of rate cuts from President Trump or the Fed, as claims to bolster housing demand are put on the back burner while inflation is at the forefront. The elevated rates and high home prices mean buyers have lower purchasing power, further slowing sales. Due to high material costs, newly constructed buildings are lagging. The limited lab supply tightens the supply even more.

ICE and Deportations of Illegal Migrants

San Diego is one of California’s largest cities and hosts a large immigrant population. In this case, the state bureaucracy indeed understands how ICE operates. It does whatever is in its power to mitigate losses, at least in the formal sense. However, sanctuary states sustain direct attacks from ICE and do face serious repercussions in terms of being targeted by the Trump administration, as federal aid is likely to be suspended during this period.

Poland Asks for Help

Poland asks for financial support from the eurozone while repeatedly failing to adhere to the criteria set by the EU. Seeking funds while carrying the additional burden of upholding immigration laws seems ludicrous. On the other hand, immigration policies that lack a clear pretext for hiring foreigners based on EU citizenship, granted that the framework exists. As for regions around the border ice, they can deploy extra agents and capture everyone else carrying border crossing passes; however, questions about why the EU allows free movement raise eyebrows. Sadly, no one cares beyond operational efficiency.

Housing Market and Stagnant Mortgage Rates

Several indicators are responsible for the default in the housing market and stagnant mortgage rates. Like other rates, lenders and mortgage companies set mortgage rates. Point blank, higher rates lead to lower profits, resulting in losses. The Trump Administration has focused more on long-term energy independence deregulation, which is suspected of easing inflation over time, and struggles with short-term relief concerns. Real estate and construction have also been stricken due to the zoning burden, high demand, and lower housing supply. In contrast to reduced profits, which would ease demand and stagnant pricing, prices remain propped up.

One can speculate on the bounds and bounds of reasoning regarding the stance on the world’s mortgage and real estate policies. Paying thoughts slim and slim towards an economy that seems to grow without bounds pushes us towards idealistic reasoning – one simple disparate change to ease legislation. Keeping up to date with the salient topics presented to us belittles us, so we drop other burdens of reality, staying with hopes that few and few wish to see.

-

GCA Forums Headline News Weekend Edition Report: May 19–24, 2025

Greetings and welcome to the GCA Forums Headline News Weekend Edition Report for May 19–24, 2025. This report aims to provide timely insights and analysis tailored for homebuyers, investors, real estate professionals, businesses, and strategists. This Edition has all the important news on mortgage rate cuts, housing market movements, other critical economic indicators, government actions, real estate investment policies, and financial news in the business world. Use our cutting-edge analysis and confidently navigate today’s complex landscape.

Mortgage Market Updates & Available Interest Rates

Mortgage rates have surged again. The 30-year fixed-rate mortgage averaged 6.86% as of May 22, 2025. This marks an increase of 0.05 percentage points from the previous week. Also, as reported by Freddie Mac and the mortgage market update published on May 22, by the 21st, rates are hitting 6.95% due to growing fears of national debt alongside bond market concerns. Most experts are still cautiously optimistic, with four of the five major housing authorities indicating a modest decline in rates for Q2 2025 and possible dips below the 6.5% mark by the year-end.

Important Key Developments

Policy Impacts:

The Federal Reserve’s decision to maintain its stance on holding core rates suggests uncertainty surrounding President Trump’s proposed tariffs (mass deportation combined with tax cuts), which could potentially inflate and keep core rates sticky high.

Lender Trends:

Fannie Mae and Freddie Mac have tightened the DTI ratio requirements, affecting more borrowers. Investors seeking flexible options continue to seek DSCR and non-QM loans.

Rate Lock Strategies:

At or near 7%, locking a rate for 45 days ensures no unforeseen spikes within that period.

Why It Matters:

Homebuyers and borrowers can save by planning strategically, as spending varies by 1.5% between lenders, depending on their readiness to borrow and credit score. Mortgage experts can use these changes to help clients select more favorable loan products, such as 5/1 ARMs for short-term owners.

Market Indicators & Housing News

Affordability is recovering with some improvement; however, the high prices and constrained stock continue to challenge buyers within the housing market. As reported by the National Association of Realtors, in March 2025, the national median home price hit $403,700, reflecting a 2.7% increase year over year.

Key Trends:

Persistently high rates make it very difficult for most first-time buyers. Still, resilience remains through FHA loan applications with lower credit standards.

Slowly increasing housing inventory presents some hope for buyers, but tight supply sustains intense competition in hot markets.

Regional Analysis:

Areas such as Austin, TX, experienced an increase in purchase applications (+11% week over week). However, coastal cities still prove difficult for buyers.

Rental Market:

The demand for multifamily home rentals is expected to decrease by 4% by 2025, but the long-term outlook remains strong because of cost-saving multifamily units.

Focus Areas:

Looking into price changes and shifts in inventory can offer good insights to homebuyers and investors about opportunistic windows. Sellers can take advantage of hot markets, and buyers are encouraged to look where there is growing inventory.

Inflation & Federal Reserve Reports

Federal officials’ current policies and the inflation rate continue to impact the housing and mortgage sectors. Constraining inflation is forecasted at 2.4% yearly, with housing costs significantly impacting this figure. No rate cuts were made in May, which points to the Fed’s concern for inflation driven by tariffs and a slow economy.

Condensed Notes of Greater Importance

CPI and PCE:

Increased spending on gas, available homes, and housing prices are projected to show three straight months of inflation growth, demonstrating ongoing price growth in these categories.

Economists’ Fed Allies Forecast:

Economists project that cuts to the housing rate cap could be implemented in mid-2025, assuming inflation eases or employment declines.

Impact of Affordability:

Median family income is projected to be $97,800 in 2024, but purchasing power continues to decline due to inflation. This directly impacts affordability when purchasing a home.

Why This Matters:

Investors and borrowers should closely examine inflation data to predict rate changes. A slowdown in economic activity may decrease interest rates, which could support homebuyer affordability.

Housing Affordability, Lending Trends, Job Market, and Other Important Economic Reports

Economic data released this week present a mixed outlook concerning the job market, directly impacting lending, home affordability, and the economy.

Key Highlights

Employment Data:

While the unemployment number remains unchanged, emerging market weakness bolsters homebuyer skepticism.

Wage vs. Home Prices:

The rate of wage increase is far slower than the increase in home prices, especially for the middle class; this severely compromises affordability.

Risks of GDP Growth Recession:

Economists are worried about potential recession risks as GDP growth declines. However, strong consumer spending provides a glimmer of hope.

Volatile Stocks:

Uncertain policies surrounding trade continue to negatively affect investors, making stock and bond yields much more unstable.

Why this matters:

Economic factors are central in mortgage application approval and other investment plans. Entrepreneurs and those looking to buy a house must pace their strategies smartly while waiting for the right economy and steady job availability.

Government Regulation Policy Changes About Housing

Continued policy changes present both challenges and opportunities in lending and housing markets.

Important News

Loan Boundaries:

FHA and conforming loans will now be pegged to $806,500 for high-cost areas in 2025, benefiting buyers.

Tax Incentives:

Plans to provide homebuyers tax credits are gaining momentum, which may increase demand.

Rent Control and Fair Housing:

New legislation regarding tenant protections with fair housing laws attempts to resolve affordability and discrimination impacts on landlords and investors.

Foreclosure Mitigation:

Existing supported initiatives are still helping homeowners default on government-issued loans, aiding in stabilizing the market.

Why It Matters:

Real estate agents and borrowers must know policy changes to avoid missing out on loan approvals and investments. Tax credits and foreclosure relief programs are extremely useful for first-time buyers.

Tips For Real Estate Investing

Real estate remains one of the top asset classes for builders to build wealth, as new buyers are looking for places to invest in a fast-moving market.

Best Techniques

Investable Markets:

Several cities, such as Austin and Phoenix, are seeing an increase in rentals and population, which is creating great yields for rental units.

DSCR Loans:

Investors are increasingly favoring DSCR loans. Angel Oak Mortgage REIT recently reported a weighted average coupon of 7.67% on new loans, confirming this trend.

Short-Term Rentals:

Airbnb markets in tourism regions are highly valued in the short term but need consistent monitoring due to regulatory changes.

Tax Strategies:

Depreciation strategies and 1031 exchanges can maximize returns for real estate investors, especially in multifamily structures.

REIT Opportunities:

While AGNC Investment’s 16% yield is attractive and qualifies them as a leading REIT, exposure should still be limited to 2-3% of portfolios for passive income purposes.

Why It Matters:

Long-term investors can capitalize on these suggestions to scout high-return markets and loan products while improving tax strategies.

Business & Financial News in Focus

For professionals and investors, the intersection of real estate with business and financial news provides essential information.

Key Stories:

Marketplace:

Mortgage rates increased as bond yields surged amid mounting concerns regarding the U.S. credit downgrade. This also marks a highly volatile week for the stock market.

Banking Sector:

Angel Oak Mortgage REIT announced a robust Q1 2025 with a year-over-year 18% growth in net interest income, showcasing strength in non-QM lending.

Crypto and Real Estate:

The use of digital assets to purchase real estate is rising, creating innovative opportunities for more technologically inclined investors.

Small Business Loans:

Stricter lending standards hurt small business lending, adversely impacting real estate developers and investors.

Why It Matters:

These trends allow for better real estate decisions, aiding investors and entrepreneurs to adapt their plans to shifting market dynamics.

The GCA Forums Headline News Weekend Edition Report for May 19–24, 2025, examines the critical factors influencing the housing and finance industries. We examine everything from increasing mortgage rates to shifting government policies and investment options. With GCA’s industry-leading analysis, homebuyers, investors, and professionals are well-prepared to tackle today’s challenges. Don’t miss out on the daily updates, and join the GCA Forums family to unlock exclusive content and network with professionals.

Check out the personalized recommendations and analysis available at the GCA Forums News site and register today!

-

GCA Forums News: Memorial Weekend Edition, May 25, 2025

Real Estate: Housing Market Encounters Challenges as Activity Declines, Prices Surge

As the National Association of Realtors noted, the sales pace for existing homes in April 2025 stagnated at 4.0 million annually, marking the slowest since 2009. This sluggish performance represents the weakest output for April in over a decade. Lawrence Yun, the association’s chief economist, indicates that the increase in mortgage rates, now exceeding 7% compared to 6.2% in Sep of 2024, is a significant barrier. While activity is slowing, home prices continue to rise and set record after record, reducing the attractiveness level of homeownership for first-time buyers. In Canada, home sales fell 9.8% in April, though there is some positive news for buyers in increasing listings. The GCA Real Estate Roundtable is buzzing with debates about whether this is a buyer’s or seller’s market–don’t miss the discussion, and add your voice!

Over the holiday period, mortgage rates saw some changes and were relatively active.

GCA Forums News post and CNET suggest that for the week after May 26, 2025, the average rate for a 30-year fixed mortgage will sit at 6.89%. This is a decline of 3 basis points from the previous week, while the 15-year fixed rate has increased to 6.11%. Other analysts foresee the rates being around 7% unless drastic actions like inflation cooling down or a weaker labor market prompt the Federal Reserve. Moreover, forum members are giving strategies for USDA loans, locking in low rates, and rate shields that could benefit rural areas. Please share if you have found other lenders that would provide better rates or seamless processes.

Market speculation is fueled by proposed policies like the 25% tariffs on smartphones drafted by President Trump if companies such as Apple and Samsung do not relocate production to America, along with his earlier proposition of turning over 40% of single-family and half of multi-family mortgages to private entities, Fannie Mae and Freddie Mac.

GCA Forums’ Finance Forum analyzes how these policies might impact affordability and investment properties. Some users recommend cash-flowing rentals in top-tier markets to mitigate high-rate disadvantages per the Great Community Authority Forums’ advice. What’s your investment strategy during these times?

Hamptons Market: Rising Inventory and a Surge in Short-Term Rentals

Along with luxury real estate trends, the Hamptons market is gradually increasing inventory, which most buyers have not had for the past few years. As highlighted by the Hamptons Real Estate Roundtable, this gives buyers more choices. Sellers must be strategically priced to avoid prolonged price haggling. Buyers should remove mortgage contingency clauses to make better offers. A new trend of short-term (2-3 weeks) rentals is developing, largely fueled by remote work adaptability and younger long-term renters traveling to multiple summer hotspots. GCA’s Luxury Living thread is conflicted about this mid-term market evolution—contribute your thoughts!

Global Real Estate: Updates from Healthcare REIT and India Market

Northwest Healthcare Properties Real Estate Investment Trust marked its territory as a stable player in the healthcare real estate market across North America, Brazil, Europe, and Australasia by announcing a $0.03 May 2025 per unit distribution payable on June 13, 2025.

At the same time, Aditya Birla Real Estate’s stock declined by Rs 131 crore in Q4 2025. Still, it rebounded 5.42% to Rs 2038.10, suggesting renewed hope for future profitability. These developments are the focus of Global Capital Advisors’ Global Markets forum: join to discuss cross-border private equity placements.

Beyond Real Estate: Entertainment, Sports, and Community Highlights

Entertainment:

At the box office, Disney’s Lilo & Stitch and Mission: Impossible

The Final Reckoning is poised to compete for the top Memorial Day spot. Inside the Gaming Guild, Fortnite’s Crew Pack skin for June 2025, Ayla Winn, has garnered mixed reviews, some calling it “fire” while others claimed it was lackluster.

Sports:

Canadian tennis prodigy Victoria Mboko turned heads at Roland Garros as she opened her campaign with a dominant 6-1, 7-6(4) win. The sports threads seem optimistic, rallying to support her against Eva Lys in the next round.

Community:

Earlier this week, severe storms struck 10 states within the U.S. GCA’s Community Corner is sharing best practices for recovery as NOAA warns of a busy 2025 hurricane season. In other news, Lady Gaga’s Abracadabra dominated Most Requested Live, and BNK48 fandoms eagerly anticipate the release of their single Colorcon Wink on May 31.

Contribute to GCA Forums’ Real Estate, Mortgage, Community threads, and more. Happy Memorial Day!

-

I spoke with James Abrams, who normally goes by JD. JD is a BDM at NEXA Mortgage, and I have known him for several years. I have heard different, if not shocking, news from JD. JD adopted a German Shepherd dog over a year ago. The dog’s name is Chloe. The German Shepherd dog Chloe is two years old. I asked JD how his German shepherd dog was doing. JD went on to tell me that his dog is doing great and how much he loves Chloe. Then he went on to tell me about an incident he had with Chloe a few months back. James said his German shepherd dog, Chloe, had ten puppies. The father of the ten puppies is not known since Chloe got out of her territory and wandered the neighborhood. The weirdest part of the story was that every time James went to check on the puppies, the number of pups was getting reduced. For example, the ten puppies he witnessed and counted, it went down to eight pups. Then seven puppies. Then five. So JD said something was up. Long story short, Chloe, the German shepherd dog that gave birth to ten puppies, was eating her own puppies with two puppies left over. Besides the ten puppies, the German shepherd Chloe at two birds, Cockatiels, that James kept as pets. I will ask James if he can share the entire story on this forum. Anyone hear of such a bizarre incident where a dog who gave birth to a large litter of puppies at the entire litter? I heard of animals eating the placentas of their newborns but not devouring the entire pup. Something is wrong with her. Any response to this thread will be greatly appreciated.

JD, I appreciate you sharing your story. I am sure you going through this bizarre incident with Chloe is not the first case among those dog lovers and owners who are either intentionally or unintentionally breeding their dogs.

-