-

HUD Chapter 13 Bankruptcy Dismissal Guidelines on FHA Loans

Posted by Brett on February 21, 2024 at 6:51 pmWhat are HUD Chapter 13 Bankruptcy dismissal guidelines to qualify for an FHA LOAN. Is there any waiting period requirements.

Gustan Cho replied 1 year, 8 months ago 6 Members · 5 Replies -

5 Replies

-

To get an FHA loan, you have to prove you have made your payments on time, on the Chapter 13 plan for at least one year. Your lender will require documentation showing all payment dates and you will need permission in writing, from the court to apply for the mortgage.

-

FHA LOANS DURING CHAPTER 13 BANKRUPTCY

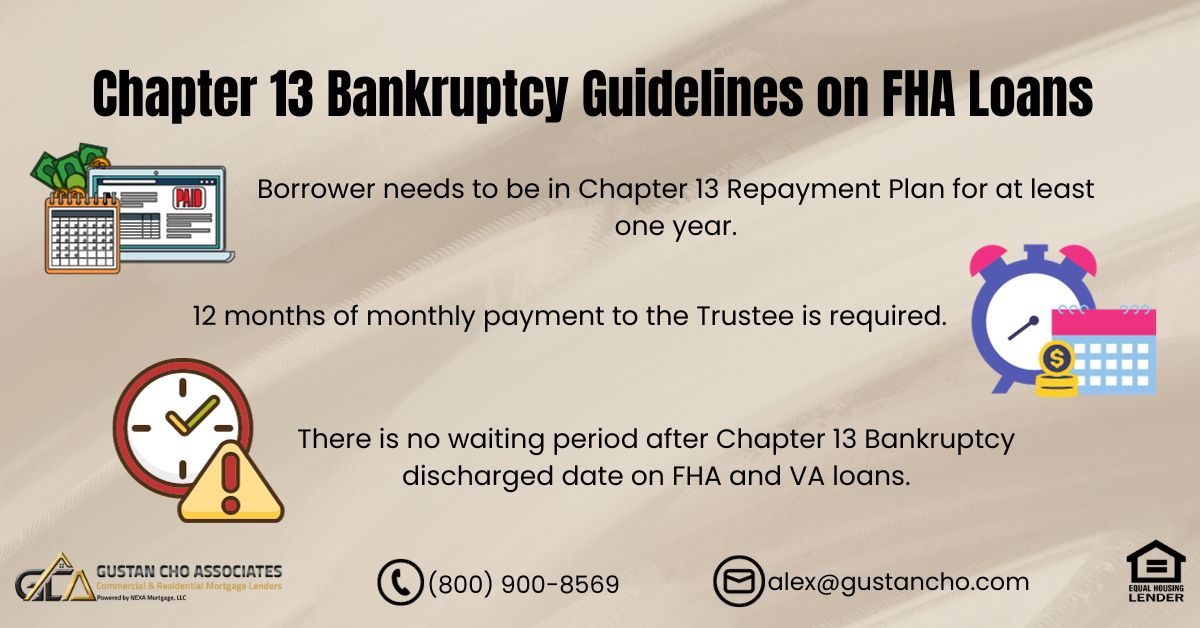

HUD Guidelines allow borrowers to get approved for FHA loans during chapter 13 bankruptcy one year into the repayment plan. The CHAPTER 13 BANKRUPTCY does not have to be discharged. Needs to be manual underwriting with Trustee Approval.

https://fhabadcreditlenders.com/fha-chapter-13-bankruptcy/

fhabadcreditlenders.com

FHA Chapter 13 Bankruptcy Guidelines

FHA Chapter 13 Bankruptcy Guidelines allow borrowers to be eligible for FHA loans one year into the Chapter 13 repayment with trustee approval

-

FHA and VA LOANS are the only two mortgage options borrowers have to qualify and get approved on home loans during Chapter 13 Bankruptcy repayment. No other loan program allow borrowers to qualify for a mortgage loan while in a Chapter 13 Bankruptcy repayment plan. Not even non-qm loans.

-

HUD’s guidelines for obtaining FHA loans during and after a Chapter 13 bankruptcy are designed to help individuals who have demonstrated financial responsibility during the bankruptcy period. Here’s a detailed overview of these guidelines:

FHA Loan Eligibility During Chapter 13 Bankruptcy

Minimum Time Requirements:

- One Year of Payments: Borrowers must have made 12 months of on-time payments to their Chapter 13 bankruptcy plan.

- Court Approval: The bankruptcy court must approve the borrower’s request for a new mortgage loan.

Creditworthiness:

- No Late Payments: The borrower must have a history of timely payments on all obligations within the bankruptcy period.

- Credit Score: While the FHA does not set a minimum credit score, most lenders prefer a score of at least 580. Some lenders may have higher requirements.

Manual Underwriting:

- FHA loans for active Chapter 13 bankruptcy borrowers are subject to manual underwriting. This means a more detailed review of the borrower’s financial situation, including income stability, employment history, and overall credit profile.

Income and Employment Verification:

- Stable Income: Borrowers must demonstrate stable and sufficient income to cover mortgage payments, living expenses, and bankruptcy plan payments.

- Employment History: A steady employment history of at least two years is typically required.

FHA Loan Eligibility After Chapter 13 Discharge

Discharge Requirements:

- Seasoning Period: Typically, borrowers must wait at least two years from the discharge date of their Chapter 13 bankruptcy to qualify for an FHA loan without manual underwriting. However, borrowers can be eligible for an FHA loan one year after discharge if they have demonstrated strong credit and financial management during and after the bankruptcy.

Credit and Financial Stability:

- Credit Improvement: Borrowers should improve their credit score and maintain a positive credit history post-bankruptcy.

- Financial Management: Demonstrating sound financial management and having no additional delinquencies or defaults post-discharge is crucial.

Documentation:

- Discharge Papers: Borrowers must provide a copy of their bankruptcy discharge papers.

- Verification of Payment History: Documentation of timely payments throughout the bankruptcy period will be required.

Key Considerations

Debt-to-Income Ratio (DTI):

- The borrower’s DTI ratio must meet FHA guidelines, which typically allow for a maximum of 43% for front-end ratios and up to 56.9% for back-end ratios, depending on compensating factors.

Compensating Factors:

- Lenders may consider compensating factors such as significant cash reserves, a substantial down payment, or other positive financial attributes that can offset the risk associated with recent bankruptcy.

Counseling Requirements:

- Some lenders may require borrowers to complete homebuyer education or credit counseling courses to ensure they understand the responsibilities and implications of taking on a new mortgage.

These guidelines help ensure that borrowers who have undergone Chapter 13 bankruptcy and demonstrated financial responsibility can still achieve homeownership through FHA loans. Always consult with a mortgage professional or financial advisor for personalized advice and to navigate the specifics of your situation.

https://gustancho.com/qualifying-for-fha-loan-during-chapter-13-bankruptcy/

gustancho.com

Qualifying For FHA Loan During Chapter 13 Bankruptcy

Qualifying For FHA Loan During Chapter 13 Bankruptcy: Borrowers can qualify for an FHA loan during Chapter 13 one year into the plan

-

FHA and VA loans are generally the only mortgage options available to borrowers still in an active Chapter 13 bankruptcy repayment plan. Here are detailed insights into why these two loan types are available and the specific requirements for qualifying under these programs:

FHA Loans During Chapter 13 BankruptcyEligibility Requirements:

One Year of Payments: Borrowers must have made 12 months of on-time payments to their Chapter 13 bankruptcy repayment plan.

Court Approval: The bankruptcy court must approve the borrower’s request for a new mortgage loan.

Manual Underwriting: Loans are subject to manual underwriting, which involves a detailed review of the borrower’s financial history, current financial status, and the reasons for the bankruptcy.

Credit and Income: Borrowers must demonstrate stable income and meet credit requirements, which vary by lender but generally require a minimum credit score of around 580.

DTI Ratio: Borrowers must meet FHA’s debt-to-income (DTI) ratio requirements, which typically allow for a maximum of 43% for front-end ratios and up to 56.9% for back-end ratios, depending on compensating factors.

VA Loans During Chapter 13 BankruptcyEligibility Requirements:

One Year of Payments: “VA Loans During Chapter 13 Bankruptcy “Similar to FHA loans, VA loans require that borrowers have made at least 12 months of on-time payments to their Chapter 13 repayment plan.

Court Approval: The bankruptcy court must approve the borrower’s request to take on new debt.

Manual Underwriting: VA loans are also subject to manual underwriting, meaning each application is carefully reviewed on a case-by-case basis.

Credit and Income: Borrowers must demonstrate sufficient income and meet the VA’s credit requirements. While there is no official minimum credit score for VA loans, most lenders prefer a score of at least 620.

VA Certificate of Eligibility: Borrowers must obtain a Certificate of Eligibility (COE) from the VA, which proves they meet the VA’s service requirements.

Non-QM Loans and Other Conventional Loans

Non-QM (Non-Qualified Mortgage) and conventional loans generally do not allow borrowers to qualify for a mortgage. At the same time, they are still in an active Chapter 13 bankruptcy repayment plan. These types of loans typically require the bankruptcy to be fully discharged or dismissed before a borrower can qualify. FHA Loans and VA Loans: Allow qualification during Chapter 13 repayment. Require at least 12 months of on-time repayment. Require court approval. Subject to manual underwriting. Have specific credit and income requirements.

Non-QM Loans and Conventional Loans: Generally, qualifications are not allowed during active Chapter 13 repayment. Require bankruptcy discharge or dismissal. Consulting with a mortgage professional or financial advisor can also provide personalized guidance tailored to individual financial situations and help navigate the complexities of obtaining a mortgage during a Chapter 13 bankruptcy repayment plan.

https://gustancho.com/fha-chapter-13-bankruptcy-guidelines/

gustancho.com

FHA Chapter 13 Bankruptcy Guidelines on FHA Loans

VA and FHA Chapter 13 Bankruptcy Guidelines allows borrowers to qualify one year into a Chapter 13 Repayment Plan via manual underwrite

Log in to reply.