-

What Happens if a Driver of a Car Rear Ended Me and I Rear Ended Someone Else

Posted by Dawn on November 21, 2025 at 1:03 pmWhat happens if a driver of a car rear ended me and I rear ended someone else. I only have liability insurance and I was not at fault. I have been getting runarounds since September 26, 2025. The other driver’s insurance company picked up my vehicle and took it to CoPart because it was demmed a total loss. Thank you.

Julio Munoz replied 3 months, 2 weeks ago 2 Members · 1 Reply -

1 Reply

-

Short Answer: Since you only carry liability insurance and you were not at fault, the at‑fault driver’s insurance should cover your damages, including the total loss of your vehicle. However, because liability insurance does not cover your own car, you must rely on the other driver’s insurer to pay. If they are delaying or giving you the runaround, you may need to escalate with a formal claim, involve your state’s Department of Insurance, or consult an attorney to protect your rights consumershield.com Forbes FindLaw.

🔎 Breaking Down Your Situation

- Rear-end chain reaction: In multi-car accidents, liability is determined by fault. If you were rear-ended first and that impact caused you to hit the car in front, the driver who hit you is typically considered at fault novianlaw.com.

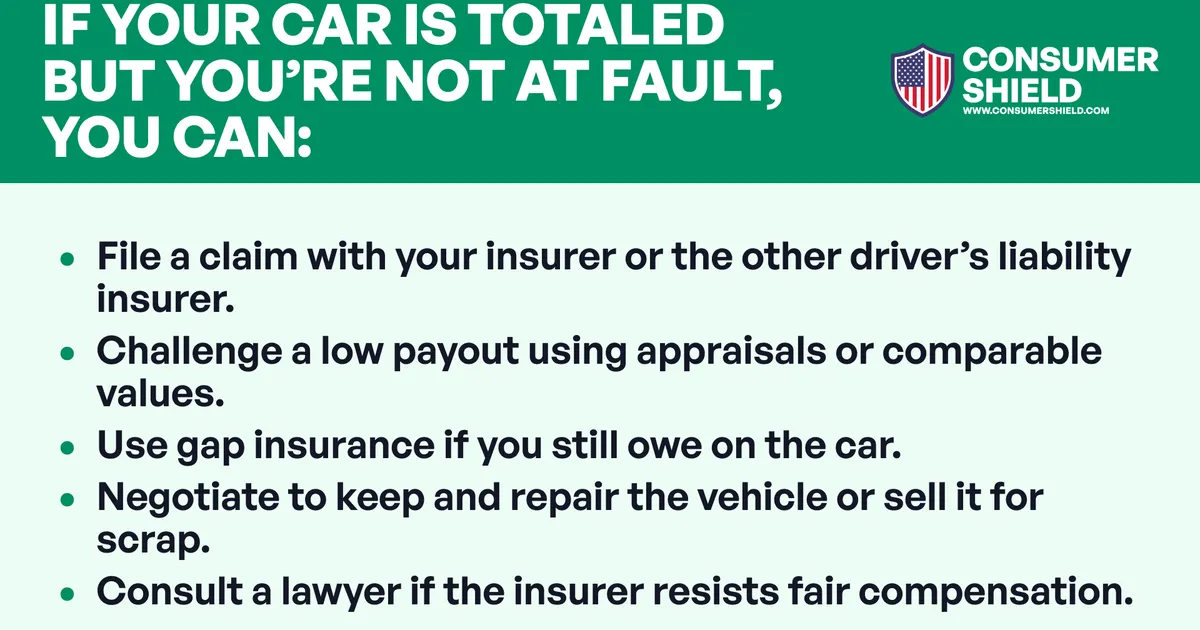

- Your coverage: Liability insurance only pays for damages you cause to others. It does not cover your own vehicle. That’s why the other driver’s insurance company took possession of your car and deemed it a total loss consumershield.com Forbes.

- Total loss process: A car is considered “totaled” when repair costs exceed a set percentage (often 70–80%) of its pre-accident value legalclarity.org. The insurer should pay you the actual cash value (ACV) of your car before the accident, minus any deductible if applicable.

🚗 What Should Happen Next

- Payout for your car: The at-fault driver’s insurer should issue you a settlement check for the ACV of your vehicle Forbes FindLaw.

- Disputes: If you believe the payout is too low, you can dispute it by providing evidence of your car’s value (recent sales, receipts for upgrades, etc.) consumershield.com.

- Delays: Insurance companies sometimes stall. You can file a complaint with your state’s Department of Insurance or seek legal help if they continue to delay consumershield.com FindLaw.

- Chain liability: You should not be held liable for the car you rear-ended if the collision was caused by the driver behind you. That liability falls on the person who hit you novianlaw.com.

📝 Practical Steps You Can Take

- Gather all documentation: accident report, photos, repair estimates, and communications with the insurer.

- Request a written explanation from the insurer about the payout timeline and valuation.

- If delays persist, file a complaint with the Illinois Department of Insurance.

- Consider consulting a personal injury/property damage attorney—many offer free consultations.

Bottom Line: With liability-only coverage, you depend entirely on the at-fault driver’s insurance to pay for your totaled car. Since they already picked up your vehicle, they owe you compensation. If they continue to stall, escalate formally—through your state regulator or legal counsel—to ensure you receive the fair value of your car.

Sources: consumershield.com Forbes legalclarity.org novianlaw.com FindLaw

Would you like me to walk you through how to dispute the insurer’s valuation if they offer you less than your car is worth? That’s often the sticking point in these cases.

-

This reply was modified 1 month, 2 weeks ago by

Sapna Sharma.

Sapna Sharma.

consumershield.com

Car Totaled but Not at Fault: What You Can Do (2026)

When an insurer classifies a car totaled, not at fault, you have several options. Learn about them and how much you stand to get paid for your loss.

Log in to reply.