-

UWM and Rocket Mortgage 1% rate buydown for free for first year

Posted by Juan on May 29, 2026 at 4:23 amhow does UWM one percent rate buydown for fist year work? From what I heard was that Rocket Mortgage offered a one percent mortgage rate buydown with NO points. I don’t quite understand how that works. From my understanding, that means the first year, the rate is reduced by 1.0$ from the going market rate and starting year two, it goes back to what the market rate is. Many unanswered questions is how does the one percent mortgage rate reduction from the market rate work? What happens year two? What mortgage rate will the borrower get? Will it be a fixed rate or adjustable rate? How does UWM 1% rate buy down with NO DISCOUNT POINTS compare to Rocket Mortgage one percent rate buydown? Again, from my understanding, Rocket Mortgage started this 1% rate buydown for the first year and UWM followed. Thank you.

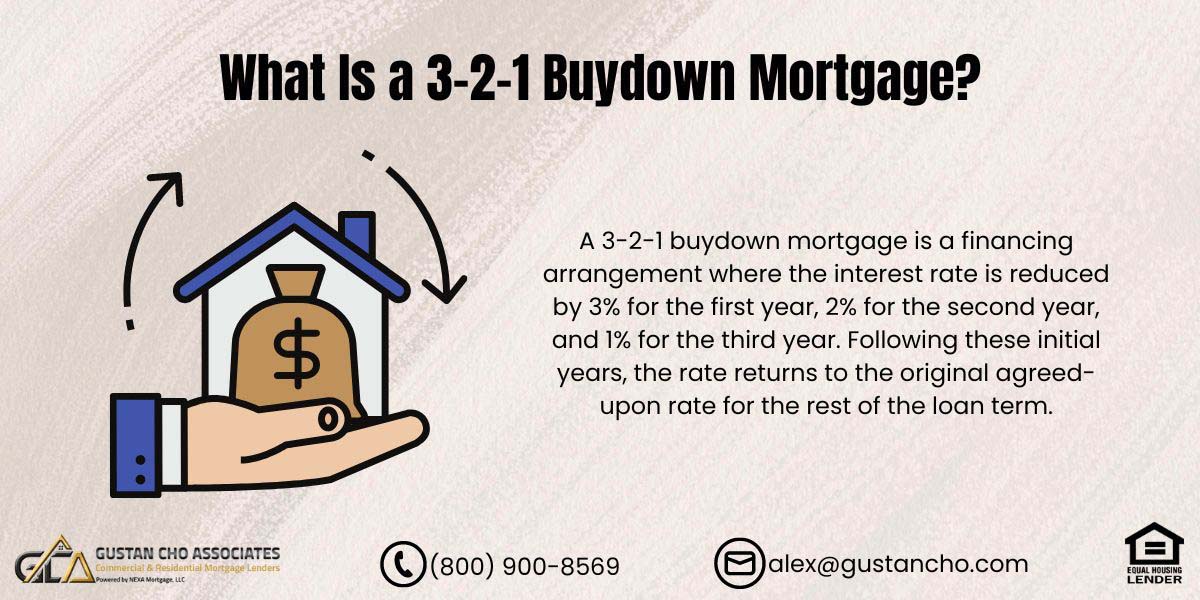

What Is a 3-2-1 Buydown Mortgage?

gustancho.com

What Is a 3-2-1 Buydown Mortgage?

A 3-2-1 buydown mortgage is a type of loan that starts out with a low rate and increases over three years until it reaches its permanent rate.

Gustan Cho replied 1 month, 2 weeks ago 5 Members · 5 Replies -

5 Replies

-

UWM’s 1% (1-0) rate buydown is a fixed purchase loan offered at no extra cost to the client (lender credit applied) on select purchase loans until June 30, 2026.

How UWM’s 1-0 Buydown Works

- You pay the note rate (the locked rate in your loan documents).

- In year 1, your monthly payment reflects a 1% reduction from the note rate, resulting in a lower payment for the first 12 months.

- UWM issues a credit to fully offset the cost, so you and the broker incur no expense (no discount points for the borrower).

- Year 2+: the payment adjusts to the full note rate.

- The loan maintains a fixed rate (or ARM), so it remains unchanged after year 1—it merely reverts to the original fixed-rate note.

Example: If your note rate is 6.5% on a $400,000 30-year fixed loan:

- Year 1: Payment based on ~5.5%.

- Year 2+: Payment based on 6.5%.

Your loan qualification is based on the full note rate (not the discounted one). This is a limited offer on both conventional loans and government-backed purchases (FHA/VA/USDA), fixed and some ARMs.

This is not a permanent rate reduction or an adjustable-rate mortgage reverting to the market rate after year 1. It is a one-year temporary cost to the lender on an otherwise fixed rate.

Rocket Mortgage’s 1% Rate Buydown

Rocket offers alternative 1-0 temporary buydowns (lender-funded or with seller/builder contributions).

- Currently, this gives a 1% discount on the first-year rate for primary/secondary retail purchase loans.

- The specifics closely match UWM’s:

- Year 1 features a lower payment, as if the rate is 1% lower; then the payment returns to the full note rate in year 2 and beyond.

- Some promotions may let the lender fund the buydown (like UWM’s free offer) or require seller concessions.

- Rocket has advertised 2-1 buydowns (bigger reductions in years 1 and 2) in the past.

UWM vs. Rocket

- Both offer a temporary 1% reduction in rate and payment for year 1, then revert to the full note rate, with limited borrower-paid discount points.

- Both restrict the offer to fixed-rate mortgage products, meaning the payment is reduced only in year 1.

- UWM offers a free lender-funded version through June 30, 2026, targeted at wholesale brokers. It’s a simple, accessible program for agency- and government-backed loans.

- Rocket is more of a retail/direct-to-consumer lender.

- Their 1-0 is available, but unlike UWM, they also endorse other products (1% down, etc.).

- UWM offers flexible wholesale pricing.

- Rocket often competes on price vs. brokers.

- Always compare Loan Estimates on price and terms.

Important Notes

- You qualify at the full note rate (lenders prefer to guarantee that you can repay the loan balance if it were to increase after year 1)

- Although the programs are great for cash flow relief, they do not affect the long-term interest rate.

- Offers have strict deadlines.

- UWM is currently granting a deal that ends June 30, 2026.

- Confirm your eligibility with your loan officer.

Eligibility often depends on factors like loan amount, credit score, and property location. Provide these details so I can help determine whether you qualify and assist you in comparing lenders’ offers to find the best deal.

-

What are the mortgage loan programs that UWM offers the 1.0% first year buydown to borrowers? FHA, VA, USDA, Conventional loans? What are the minimum requirements and eligibility requirements? Is the UWM 1.0% mortgage rate buy down for the first year a lender paid or borrower paid compensation program for mortgage loan originators? Does the mortgage broker take a compensation hit under 2.75% yield spread premium?

-

UWM’s Free 1-0 Lender-Paid Temporary Rate Buydown is available from May 6 to June 30, 2026, for agency purchase loans, including conventional and government options such as FHA, VA, and USDA, provided they meet UWM and agency guidelines.

UWM 1-0 Buydown: Basic Program Terms

- In the first year, UWM reduces the borrower’s interest rate by 1%, lowering payments at no cost to the borrower or broker.

- UWM covers the buydown cost with a lender credit.

Publicly Stated Requirements Include:

- This promotion applies only to purchase loans.

- UWM does not offer this lender-paid buydown for any refinancing.

- Eligibility is limited to agency products, including conventional and government-insured loans such as FHA, VA, and USDA.

- Both fixed and adjustable-rate purchase mortgages are eligible.

- Loan terms from 8 to 30 years qualify for this program.

- New loan locks are accepted from May 6 to June 30, 2026, during the offer period.

- The Control Your Price program is not eligible for this promotion.

LLPA Credit UWM Is Applying

- UWM applies a 0.875 LLPA credit for loan terms of 16 to 30 years.

- A 0.750 LLPA credit applies to loan terms of 8 to 15 years.

- UWM states that the lender credit fully offsets the cost of the 1-0 temporary buydown.

Minimum Borrower Requirements

UWM does not specify minimum FICO scores, debt-to-income ratios, reserves, loan-to-value ratios, occupancy, or automated underwriting requirements for the 1-0 buydown.

- Borrowers must meet standard criteria for their loan type.

- For Conventional, the file must satisfy the requirements of both Fannie Mae/Freddie Mac and UWM.

- For FHA, the file must satisfy FHA and UWM requirements.

- For VA, the file must satisfy VA and UWM requirements, including VA residual income and entitlements.

- For USDA, the file must meet USDA and UWM requirements, including property eligibility, income limits, and USDA approval.

- Borrowers must qualify based on the full note rate and payment, not the reduced first-year payment.

- The permanent interest rate remains unchanged.

Is It Lender-Paid or Borrower-Paid?

- The Free 1-0 Lender-Paid Temporary Rate Buydown is free for borrowers and brokers, as UWM covers the cost through a lender credit.

- UWM confirms that the borrower does not pay for this program.

Clarification is Needed on Whether the Program Affects Lender Paid or Borrower-Paid Compensation for Mortgage Loan Originators (MLOs).

In this context, “lender-paid” refers to the temporary buydown cost, not to the broker compensation structure.

While the program is a lender-paid buydown, it does not determine whether broker compensation is lender-paid or borrower-paid. Regulation Z prohibits compensation from varying based on loan terms or proxies. Dual compensation rules apply if the consumer pays the loan originator directly.

This Raises the Question of Whether Broker Compensation is Reduced Under the 2.75% Yield Spread Premium (YSP) Structure.

UWM states brokers should not lose compensation due to the free 1-0 lender-paid buydown. There is no extra cost to the broker, as the credit covers the buydown.

However, UWM does not publicly disclose how this program affects a broker’s exact 2.75% lender-paid compensation or YSP. These details are likely available through UWM’s broker portal, rate sheets, compensation agreements, or account executive guidance.

In summary, UWM’s public statements indicate the buydown should not reduce broker compensation. However, verify individual cases in EASE or with a UWM account executive if compensation appears below the expected 2.75%.

Key Questions for UWM Include:

- “Will the Free 1-0 Lender-Paid Temporary Rate Buydown LLPA credit maintain my total 2.75% LPC compensation, or can it also lower broker compensation on loans where the maximum premium is less than 2.75%?”

- UWM’s free 1-0 first-year temporary buydown is available for agency purchase loans, including Conventional, FHA, VA, and USDA, if the loan meets agency and UWM guidelines.

- The lender pays the buydown cost, not the borrower.

- UWM’s public statements indicate there is no cost to the borrower or broker, and broker compensation should not decrease as a result of the buydown.

- However, review UWM’s live pricing and compensation agreements to confirm the impact on the 2.75% YSP or lender-paid compensation, as this is not fully detailed in public announcements.

-

The free 1.0% buy down the first year seems to be a great deal with no hidden fees or tricks. I will research this product more tomorrow and post my findings.

-

Hi Gustan,

If you’re working with clients who feel stuck between staying put and making their next move, HomeLight’s Buy Before You Sell (BBYS) paired with UWM’s 1-0 lender-paid buydown can be a powerful solution.

BBYS helps qualified homeowners purchase their next home before selling their current one, while UWM’s buydown can help ease payment concerns during the first year.

If you’d like to see how this works in action, we’re hosting HomeLight Office Hours with UWM this Thursday at 10:30am PST. It’s a live, small-group Q&A where we’ll walk through the BBYS program and answer questions in real time: Register here.

Feel free to call, text, or email me anytime, or click here to schedule a time to connect.

Thank you,

Kara Kleingarn

Lender Sales Manager

Direct (623) 526-0205

Log in to reply.